As mortgage rates rise, is money to be made in renting?

By Sam Slator on 25 January 2023 in Property

For the past decade or so, I’ve been lucky enough to have almost interest-free mortgage payments. Having taken out a tracker mortgage in 2007 (when the interest rate was 5.5%), the sudden fall to emergency levels following the global financial crisis, was very kind to my wallet.

The last few months have seen something of a sharp reversal. With interest rates now at 3.5% and rising, my monthly payments have increased quite substantially – at a time when all my other bills are rising too.

Can you afford to own a house?

While rising interest rates can be an issue for homeowners, they also mean that for many, the prospect of buying your first home is even more of a challenge than it already was.

The latest data I could find at the Office of National Statistics dated back to March 2021, when the average house sold in England cost the equivalent of 8.7 times the average annual disposable household income, while in Wales it was 6 times and in Scotland 5.5 times*. With mortgage rates so much higher today, these ratios will only have increased.

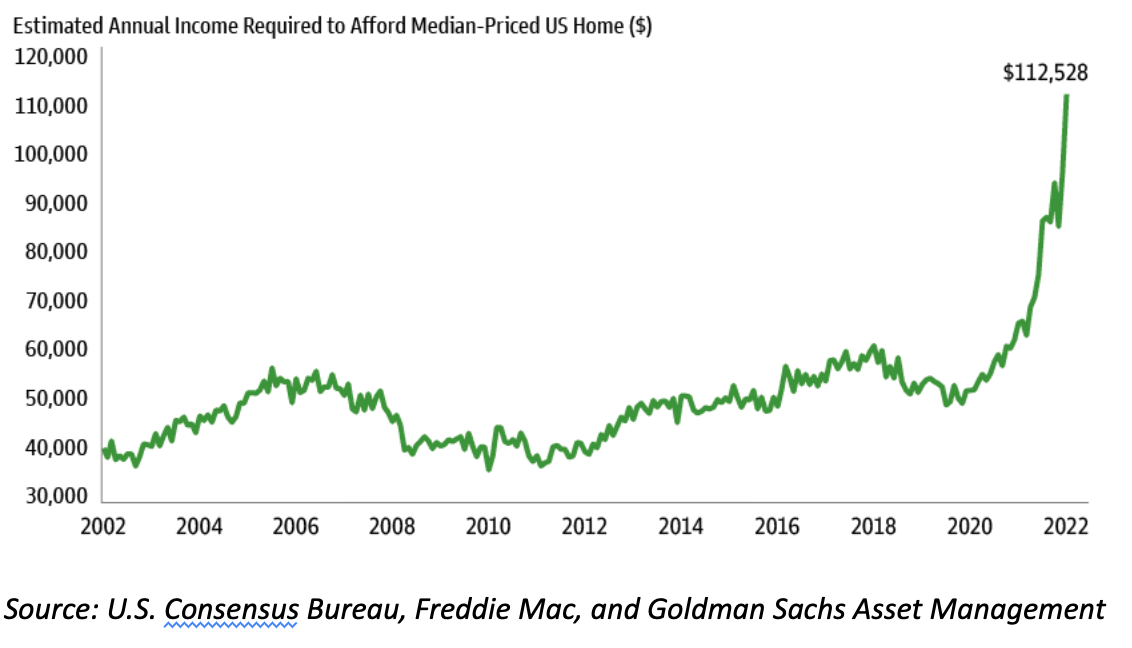

The situation in the US is similar – as shown dramatically in the graph below. The estimated annual income required to afford a median-priced US home has sky-rocketed.

Along with the chart, which was put together by Goldman Sachs Asset Management, was the comment: “Long considered a key pillar of wealth creation, home ownership in the United States has shown its teeth as mortgage rates have more than doubled over the previous twelve months. In our estimate, servicing the costs of owning a home in today’s market has increased by 71% from the year prior.”

Rathbones recently reported a similar story, saying the recent dip in US economic data follows on from a huge and sustained fall in US home sales. “This drop in real estate activity is to be expected when the average rate on the standard 30-year mortgage has ballooned from 3.1% at the start of 2022 to 6.2% today,” the company stated.

Will the housing market fall in a recession?

Now, with recession looming, you could argue that house prices will fall, offsetting some of the problem. But will they fall far enough?

Eva Sun-Wai, co-manager of the M&G Global Macro Bond fund, says that real estate downturns (defined as two consecutive quarters of falling prices) have already been triggered in a number of economies including Canada, Australia, New Zealand, and the Nordics.

“One area where this trend is playing out most rapidly is Sweden, where house prices are falling at one of the fastest rates in the world,” she said. “House prices are now down around 15% from their 2022 peak (and apartment prices by 14%), with many economists expecting a 20% peak-to-trough decline in the HOX Valueguard index (which combines apartments and houses). Some are even saying this is too conservative.”

But Eva says that whilst the pace of the plunge is alarming, it is not all bleak. “Sweden does not have a buy-to-let market, for example, which reduces the volatility of house prices. A shortage of housing should also provide a cushion in many local markets,” she added.

And according to Rathbones, in terms of prices, US houses have yet to recede from the huge gains of the past couple of years. “And, luckily for American homeowners, virtually all of them have long-term fixed mortgages of 10, 20 years or more, so higher interest rates only really hurt those who want to move,” it stated. In fact, less than 1% of mortgage holders will experience higher interest costs in 2023 compared with last year*.

Investment opportunities in the rental sector

So, while current homeowners, by and large, may be able to cope with the interest rises, what about those still dreaming of becoming homeowners? Will more people rent rather than buy? And if they do, are there investment opportunities to be had, particularly in real estate investment trusts?

Drew Schaffer, an investment analyst at First Sentier, says that changing demographic and lifestyle preferences of people in their late 20s and early 30s, coupled with a lack of savings among people in this group and rising mortgage rates, points to an expanding renter market in the United States.

“People are getting married later – 32 on average compared to 22 years old in the 1970s. Meanwhile, this next generation of would-be homeowners are graduating college with the highest levels of student debt on record; almost half of millennials having no down payment savings at all, according to the US Census Bureau.

“These demographic shifts are set against the backdrop of higher mortgage rates and affordability ratios not seen in 20 years. This confluence of factors is likely to expand the renter market in the US, which could present an opportunity for investors.”

Drew’s colleague, Stephen Hayes, head of global property securities at First Sentier Investors agrees: “We are positive on the residential-for-rent sector, which includes apartments, detached housing, pre-fab homes and student housing,” he said. “The risk-adjusted returns currently offered by the sector are compelling as residential assets typically deliver stable cash flows through the cycle.”

Ji Zhang, manager of the Cohen & Steers Global Real Estate Securities fund, also told us recently that the team has a preference for assets with shorter lease durations and pricing power. “In particular, we see the residential sector benefiting from insufficient supply and home affordability issues in the for-sale market, leading to higher demand for rental housing, especially within single family homes,” she said. The fund currently has 16.7% invested in the residential sector**.

Europe also has a strong rental culture and Marcus Phayre-Mudge, manager of the CT European Real Estate Securities fund, has been a fan of the German rental sector in particular for a number of years. “In Germany rents are regulated and they have huge safety nets,” he said. The fund currently has 14.5% invested in German residential businesses, as well as a 3.7% allocation to student accommodation and 2.2% in Nordic residential opportunities**.

*Source: Office for National Statistics, House Price Affordability, Great Britain

**Source: fund factsheet, 30 November 2022

Photo by Jon Flobrant on Unsplash

This article is provided for information only. The views of the author and any people quoted are their own and do not constitute financial advice. The content is not intended to be a personal recommendation to buy or sell any fund or trust, or to adopt a particular investment strategy. However, the knowledge that professional analysts have analysed a fund or trust in depth before assigning them a rating can be a valuable additional filter for anyone looking to make their own decisions.

Past performance is not a reliable guide to future returns. Market and exchange-rate movements may cause the value of investments to go down as well as up. Yields will fluctuate and so income from investments is variable and not guaranteed. You may not get back the amount originally invested. Tax treatment depends of your individual circumstances and may be subject to change in the future. If you are unsure about the suitability of any investment you should seek professional advice.

Whilst FundCalibre provides product information, guidance and fund research we cannot know which of these products or funds, if any, are suitable for your particular circumstances and must leave that judgement to you. Before you make any investment decision, make sure you’re comfortable and fully understand the risks. Further information can be found on Elite Rated funds by simply clicking on the name highlighted in the article.

Related insights

Is 2026 the year property fights back?

Upside vs. Downside: how to judge if a fund really outperforms

Winter 2025: the funds gaining and losing their Elite Ratings