Bank of Japan: does a new Governor mean new opportunities?

By Darius McDermott on 3 April 2023 in Equities, Asia/Emerging Markets

There’s a changing of the guard in Japan this month. On 9 April, Kazuo Ueda will succeed Haruhiko Kuroda as the new governor of the Bank of Japan.

Mr Kuroda has been governor since 2012 and his time was marked by radical monetary stimulus policies designed to induce inflation in Japan and break the deflationary cycle.

But what do we know about the new Governor? And what could his tenure mean for investments in Japan? We garnered the views of seven Elite Rated fund managers.

What approach will the new Governor take?

“We expect Mr. Ueda, to adopt a more balanced approach,” said Sophia Li, co-manager of the FSSA Japan Focus fund. “Japan’s yield curve control and negative interest rate policy have been largely ineffective in rejuvenating the economy, as loan growth and inflation remain low.

“The Bank of Japan already owns more than 50% of the Japanese government bond market, which shows the strategy’s waning efficacy, and the negative interest rate policy has hurt the profitability of domestic financial institutions. Therefore, we wouldn’t be surprised if Mr. Ueda gradually abandons these strategies.”

| What is yield curve control? This is when a central bank targets a longer-term interest rate, then buying or selling as many bonds as necessary to hit that rate target. This is different to the UK and US way of managing interest rates whereby they try to control short-term rates instead. |

“Kazuo Ueda has a lot to ponder,” agreed John-Paul Temperley, co-manager of the AXA Framlington Japan fund. “His predecessor has spent equivalent to 11% of GDP defending Japan’s yield curve target. This is unsustainable. With Japanese wage inflation running hot, there is less scope for Mr. Ueda to blame price increases on temporary factors. We expect he will do something later this year. Most likely scrap the yield curve controls altogether or end the negative interest rate policy.”

“Early indications appear to be that Mr Ueda acknowledges the current ultra-loose policy is not sustainable but is unlikely to rush through changes,” added the managers of the T. Rowe Price Japanese Equity fund. “Core CPI rose at an annual rate of 3.1% in February, sharply down from 4.2% in January, although this was widely expected given the impact of government subsidies. Elsewhere, signs of wage increases coming through is encouraging for Japan and also supportive of policy normalisation.

“With that said, the recent stresses in the banking system within the US and Europe may have some spillover effect globally. In the case of Japan, this may give the Bank of Japan reason to delay any potential changes to monetary policy whilst the banking situation unfolds as the knock-on effects are likely to add some strain to the global economy and ultimately Japan.”

Richard Kaye, co-manager of the Comgest Growth Japan fund, does not agree.

“The first thing that anyone needs to know about Mr Ueda is that he is famous in Japan, for his Tokyo University ‘Ueda Zemi’ classes, which teach the unorthodox financial policy many of the younger generation of Bank of Japan and Ministry of Finance officials have endorsed,” he countered.

“The economic context that Mr Ueda finds himself inheriting suits a continuation of this unorthodox policy. Japan’s consumer price index slowed to 3.1% in February from 4.2% in January, the yen oil price has fallen over 30% in recent months and Japan government bond 10-year yields have returned to around mid-December levels.

‘Furthermore, the majority of Japanese workers are in small companies not represented by unions and limited for tax optimisation reasons in their scope to raise wages. Separately, these companies, like the government of Japan, are large borrowers who need low rates. In this context, Governor Kuroda’s comments after the last monetary policy meeting make sense; ‘no rate changes even in 2024’.

‘Since most foreign investors could not visit Japan for almost four years during Covid, a misperception festered that Japan must somehow follow the monetary path of western economies. Japan’s bank index outperformed America’s nearly 50% over the last year, in anticipation of this. We think that is all wrong.”

“We know little about the new Governor’s policy ideas,” said Sam Perry, manager of the Pictet Japanese Equity Selection fund. “He has been on record stating that Kuroda’s policy seemed to be “reaching its limits”. On the other hand, in a piece in the Nikkei last year, he argued that, while the Bank of Japan must consider normalising policy soon, it must not repeat the mistakes of the 2000s by raising interest rates too soon.”

“We can, however, sketch out a likely path. The deflationary mindset has been broken. Wage growth has strengthened. Companies can set higher prices and — for the first time in decades — are taking the opportunity to do so. Clearly, there is now little reason to maintain the yield curve control. We expect that it will be incrementally unwound before being abandoned entirely later this year.

“The hurdle to lifting the Bank of Japan policy rate is much higher. Prof. Ueda’s memories of the early 2000s and the Japanese banking crises are clearly still fresh.

Hikes in interest rates are likely some time away. We are confident that we will continue to see negative real rates in Japan and that will continue to be a positive driver for growth of the economy and the equity market.”

What could this mean for the Japanese stock market?

Scrapping the current policies should be good news for financials, according to John-Paul Temperley. “We have added to banks and diversified financials into weakness caused by the Silicon Valley Bank and Credit Suisse crises,” he said.

“Japan is pretty insulated from the fall out elsewhere and Japanese corporates are also addressing their over capitalised balance sheets. Cash piles are in scope as a combination of activist investors, the government and the stock exchange are pressuring companies to use their assets more efficiently. Announcements of large buybacks and dividend hikes are commonplace in Tokyo now.

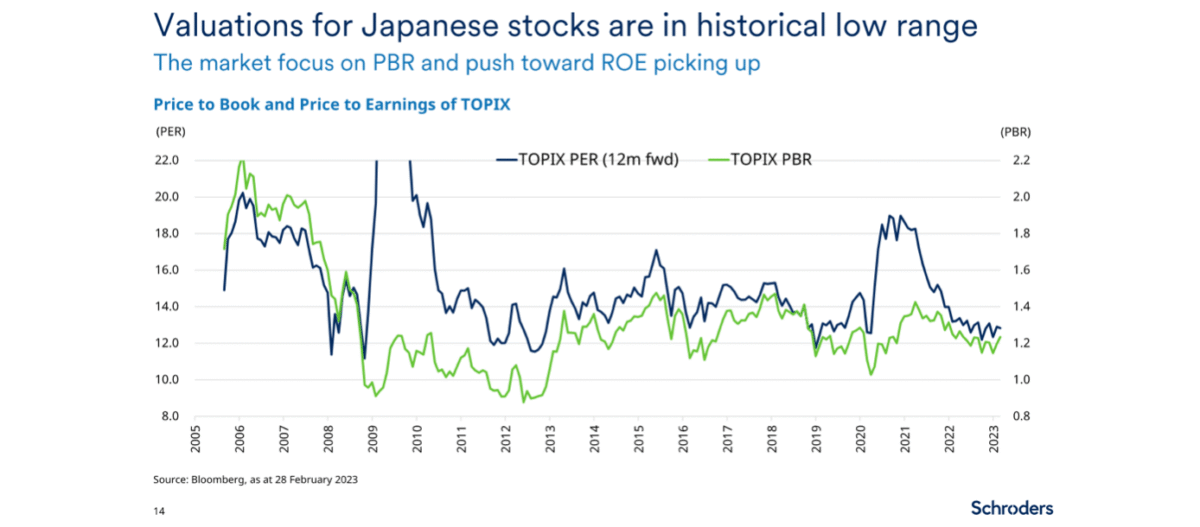

“The market is cheap and looks under owned. As tourist numbers soar since Japan reopened last October, there may be a renewed interest in the investment landscape there too. Even domestic investors are getting a boost as tax efficient savings thresholds are rising. It’s time to take a look.”

Praveen Kumar, manager of the Baillie Gifford Shin Nippon trust, says that speculation about the new governor’s actions could weigh on share prices in the short term, but if you focus on just the numbers, Japan looks very attractive.

“You are getting a host of companies growing at 20-25% who are getting larger in the market, but their starting valuations are in the low to mid-teens range,” he said. “A lot of these companies – mostly in the manufacturing side – are starting to take shareholder returns a lot more seriously. You’re seeing significant dividend payments and share buybacks. It all looks quite positive,” he concluded.

What will happen to the yen?

“Some investors will worry about the impact of the policy change on the strength of the yen and the negative impact it might have on earnings, particularly for exporters,” commented the team behind the M&G Japan fund. “We believe this is an overreaction. We don’t have a view on the yen – it may or may not strengthen in 2023, but over the long term we believe the stock market will be driven by earnings, not the level of the currency.”

“There remains a great deal of uncertainty in the macroeconomic environment at present, but we feel this is more than reflected in the valuation of Japanese equities, added the T. Rowe Price Japanese Equity team. “The multi-decade weakness of the yen has been a big factor for performance but, as we saw in the fourth quarter of 2022, headwinds like this beginning to ease can be a significant tailwind for the market.

“Despite the uncertainty in the global economy at the moment, Japan’s corporates continue to buy back stock and return capital to shareholders at record levels. This is an encouraging sign about the health of the corporates, as well as signaling the ongoing improvement in corporate governance at the company level in Japan. We believe the relentless pressure of late creates opportunity for long-term investors”.

Photo by JJ Ying on Unsplash

This article is provided for information only. The views of the author and any people quoted are their own and do not constitute financial advice. The content is not intended to be a personal recommendation to buy or sell any fund or trust, or to adopt a particular investment strategy. However, the knowledge that professional analysts have analysed a fund or trust in depth before assigning them a rating can be a valuable additional filter for anyone looking to make their own decisions.

Past performance is not a reliable guide to future returns. Market and exchange-rate movements may cause the value of investments to go down as well as up. Yields will fluctuate and so income from investments is variable and not guaranteed. You may not get back the amount originally invested. Tax treatment depends of your individual circumstances and may be subject to change in the future. If you are unsure about the suitability of any investment you should seek professional advice.

Whilst FundCalibre provides product information, guidance and fund research we cannot know which of these products or funds, if any, are suitable for your particular circumstances and must leave that judgement to you. Before you make any investment decision, make sure you’re comfortable and fully understand the risks. Further information can be found on Elite Rated funds by simply clicking on the name highlighted in the article.

Related insights

Autumn 2025: the funds gaining and losing their Elite Ratings

What explains Japan’s popularity?

Backing Japanese smaller companies for a comeback