Global dividends: down but not out

The latest Global Dividend Index from Janus Henderson suggests that dividends around the world could fall by between 15% and 35% on aggregate this year^, with the outlook for different countries varying quite considerably, depending on the extent of epidemic, the severity of lockdown, policy response, regulation, sector mix, dividend seasonality and dividend policy.

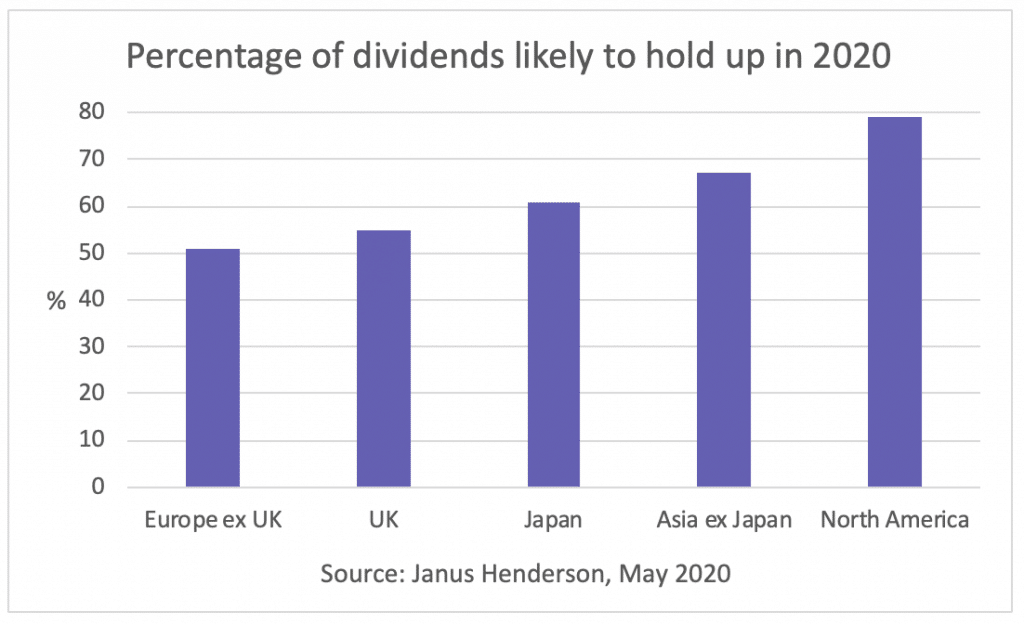

But while dividends may be scarce, they will not disappear completely, as the chart below shows. And fund managers who are able to discriminate between companies that face a lengthy dividend drought and those that could maintain or even grow their pay outs, will be in a much stronger position to deliver stronger and more sustainable growth in dividends for their investors over time.

Here, we give a quick round up of the prospects for each region:

Europe: banking dividend cuts knock $1 in $7 off payouts

Europe is likely to be the worst hit region this year, as most European companies pay their dividends in one go – so a dividend cancellation has a disproportionate impact. The European Central Bank’s prohibition on banking dividends is also expected to knock $1 in $7 off European payouts in 2020^, while other sectors taking advantage of government support schemes may find it politically difficult to pay dividends. So not only have 2019’s distributions been cancelled, but 2020’s are likely to be hit by the crisis too.

Within the continent, Janus Henderson expects Swiss dividends to see the smallest impact, as most pharmaceutical dividends have already been paid. Germany too looks relatively positive. France and Spain could face the greatest impact, thanks to the dominance of banks and insurers in the latter’s economy. George Cooke, manager of Montanaro European Income fund, however, is positive about the prospects for dividends to be reinstated. He talked in more detail about the outlook for European dividends in this video interview:

UK: Shell relinquishes the world’s top spot for dividends

The UK has already experienced a swathe of dividend cuts, including Shell, which made its first cut since World War 2, reducing its payout by two thirds. It will relinquish its position as the world’s largest dividend payer this year as a result^.

In a recent podcast, Dr Niall O’Connor, manager of Brooks Macdonald Defensive Capital fund, said: “What I think the market really hasn’t fully factored in is how low dividends are forecast to stay. Dividend futures are suggesting that the UK equity yield for 2025 will only be 3%, and obviously UK income investors have been used to between 4% and 6%.”

However, Adrian Gosden, manager of GAM UK Equity Income, says the recent sell-off has opened up some very interesting opportunities, with a view to making good money over a two-year view. He’s concentrating on making calls on management and company ‘DNA’ to determine which dividends will continue to be paid in a consistent and generous way going forward.

Emerging markets: less regulatory pressure

When most people think of emerging markets, it’s for their growth prospects. But, as Edmund Harriss, co-manager of Guinness Emerging Markets Equity Income fund, told us in his podcast this week, income opportunities are plentiful, and he is quite optimistic about dividend payments. “Within the emerging markets universe, you have quite a diversity of economies and companies, all at very different stages of development with different economic drivers,” he said.

“I think the main threat to dividends in emerging markets today is the ability of companies to operate. So you need companies with strong balance sheets. And that is something that is reflected across the world. What we’re not seeing in the same way is the regulatory interventions where banks, for example, across Europe, the US, and the UK have been instructed not to pay dividends, not to buyback shares and so forth. That is not something that is so evident in emerging markets.”

Asia: limited impact this year but possible cuts in 2021

Janus Henderson says that while Asian dividends are likely to see limited impact this year as pay outs largely relate to 2019 profits, there could be a greater impact in 2021 when weakened 2020 profits are announced. However, Asian companies tend to hold higher levels of cash, reflecting memories of the Asian crisis and traditionally higher levels of family ownership.

It’s also expected that Japan will see a smaller impact than the UK or Europe due to a lower starting payout ratio and the fact that balance sheets are very often conservative with a high proportion of companies having no debt at all. The direct economic impact has also been less severe. However, as Japan is more vulnerable to a global downturn, there may be more impact on dividends in 2021.

Richard Sennitt, manager of Schroder Asian Income fund, has currently skewed his portfolio more towards developed Asia, with holdings skewed towards Hong Kong, Taiwan, Australia, Singapore and South Korea*. The sector split shows an overweight to technology companies, real estate and materials, while financials and consumer discretionary are underweight*. Schroder Oriental Income investment trust also has around it can fall back on if necessary.

North America: tech companies pay $1 in $7 of US dividends

US companies spend more of their free cash flow buying back their own shares than they do on dividends. As a result, in the US, share buybacks, rather than dividends, are bearing the brunt of moves by management to preserve capital. The sector mix in the US is also relatively favourable. For example, technology companies are among those less impacted by the pandemic and they pay $1 in $7 of US dividends, compared to $1 in $20 in the rest of the world^. The US healthcare and consumer basics sectors also contribute more to US dividends than elsewhere, with both likely to weather the crisis better. The biggest risk is that with virus cases still rising, a second lockdown is required.

JPM US Equity Income fund holds dividend aristocrat Johnson & Johnson’s in its top ten*. It also holds Microsoft*, which is still on track to become the world’s largest dividend payer this year – having been the 25th largest 10 years ago. Manager Clare Hart believes the US economy will recover but it will first need time to heal. “Through the volatility we continue to increase quality, focus on high-conviction stocks and take advantage of market dislocations for compelling stock-selection opportunities,” she said.

^Source: Janus Henderson Global Dividend Index May 2020

*Source: fund fact sheet, 31 May 2020

This article is provided for information only. The views of the author and any people quoted are their own and do not constitute financial advice. The content is not intended to be a personal recommendation to buy or sell any fund or trust, or to adopt a particular investment strategy. However, the knowledge that professional analysts have analysed a fund or trust in depth before assigning them a rating can be a valuable additional filter for anyone looking to make their own decisions.Past performance is not a reliable guide to future returns. Market and exchange-rate movements may cause the value of investments to go down as well as up. Yields will fluctuate and so income from investments is variable and not guaranteed. You may not get back the amount originally invested. Tax treatment depends of your individual circumstances and may be subject to change in the future. If you are unsure about the suitability of any investment you should seek professional advice.Whilst FundCalibre provides product information, guidance and fund research we cannot know which of these products or funds, if any, are suitable for your particular circumstances and must leave that judgement to you. Before you make any investment decision, make sure you’re comfortable and fully understand the risks. Further information can be found on Elite Rated funds by simply clicking on the name highlighted in the article.