How responsible are your investments?

By Ryan Lightfoot-Aminoff on 18 May 2022 in Sustainable investing

Over the past few years, investors have started to focus not just on investment returns, but on how these returns are made and what impact they could be having on society and the environment.

The origins of ethical investing

Ethical investing has, in fact, been around in the UK for thirty years or so, but it’s only in the late teens and 2020s that it really started to gain momentum.

It started with negative screening: avoiding companies that are involved in ‘bad’ businesses, like tobacco and alcohol producers, animal testing, gambling, and the like. Then came positive screening, where companies with good environmental, social and governance practices (ESG) are favoured.

Understanding how fund managers view ESG risks

Today, the range of funds investing responsibly has increased dramatically – either with new launches or old funds getting a make-over.

And as their popularity has surged so have the parameters of ESG investing, with each manager doing something different.

This means it can be very difficult for investors to know exactly how responsible a fund really is.

A survey conducted by the Association of Investment Companies last year* showed that a lack of trust in asset managers’ ESG claims remains a barrier to investment, with 27% of those who don’t currently consider ESG stating that they are not convinced by such claims.

The difficulty of researching ESG-focused investments is another barrier to wider acceptance, because a majority (57%) * of all respondents agreed with the statement: “I am supportive of ESG investing, but I find these investments harder to research.”

This is also a problem for financial advisers. According to the AIC, the majority of advisers they surveyed (58%) * agreed with the statement “I am supportive of ESG, but I find it hard to research investments’ ESG policies and credentials.”

Responsible investing at FundCalibre

FundCalibre launched its Responsible Investing sector in 2015 – highlighting the funds in this category that our research team believe to be among the very best.

Now, FundCalibre has gone one step further and has included an ESG assessment on each Elite Rated and Radar fund note.

To keep things simple, each fund has been labelled as either ESG ‘Explicit’, ESG ‘Integrated’ or ESG ‘Limited’.

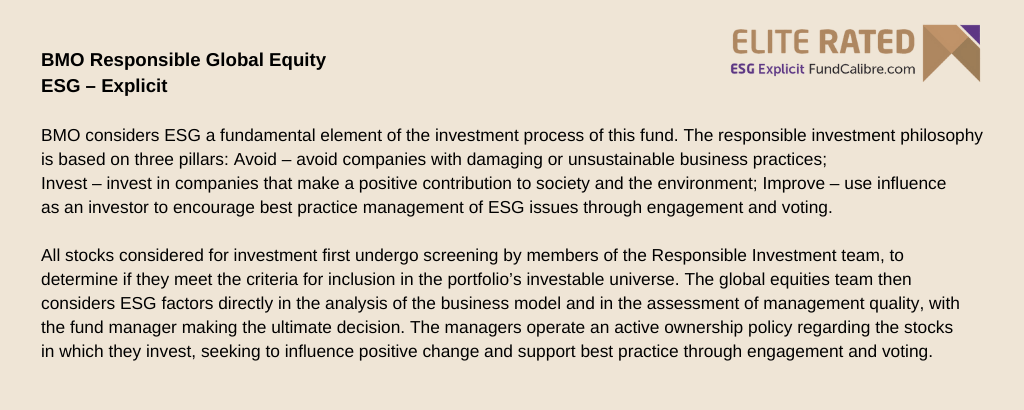

ESG – Explicit

ESG – Explicit funds are those that have an ESG/sustainable approach at the forefront of their investment philosophy. The managers will go above and beyond simple integration, with an ESG filter used as a primary feature on the investable universe, and with ESG considerations having a fundamental impact on the stock selection process.

Funds in this category are likely to have an independent panel or consumer survey to determine ESG criteria and they will either actively avoid (negatively screen) certain companies or industries, and/or will actively target (positively screen) certain ESG characteristics.

All three environmental, social and governance factors will need to be considered when building the portfolio and there must be ongoing engagement with investee company management.

The wider asset management company must be a signatory to an ESG appropriate body.

For example:

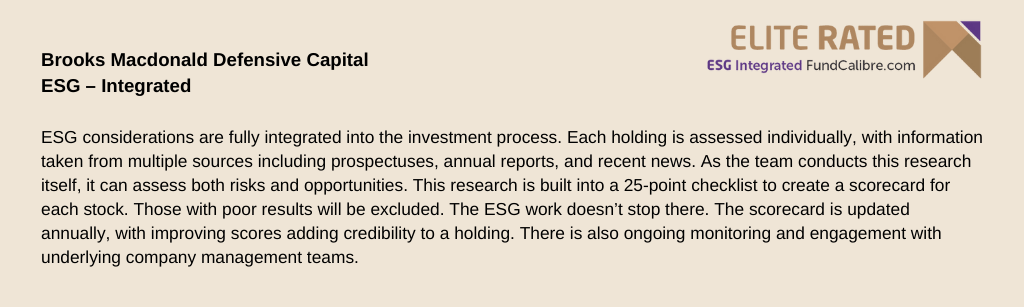

ESG – Integrated

ESG – Integrated funds are those that embed ESG analysis within the investment process, as a complementary input to decision making.

The investment universe will not necessarily be restricted in any way, but later analysis will be used to enhance the final investment decisions.

At least two environmental, social and governance inputs will need to be considered before permitting a stock into the portfolio.

Managers that hold stocks that have questionable ESG credentials will need to evidence strong rationale for including the stock in the portfolio and show that extra analysis has been undertaken to accommodate the ESG risk.

The wider company will need to be a signatory to an ESG body.

For example:

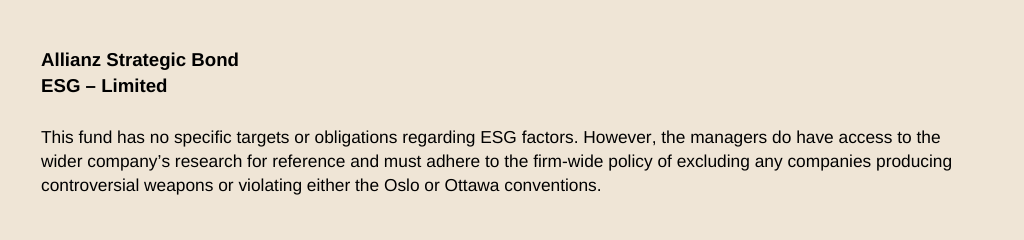

ESG – Limited

Funds in this final category are those where the overall portfolio will not be materially influenced by ESG.

These funds may still have some element of ESG in their process or be managed by a company that enforces certain negative screens, but the overall portfolio will not be influenced by ESG.

For example:

*Source: online surveys of 454 private investors and 210 financial advisers and discretionary were commissioned by the Association of Investment Companies (AIC) and conducted by Research in Finance. Investor respondents were mixed by age and gender, investable assets, and region but all had at least some money to invest and owned at least one investment product. The professional respondents comprised 125 financial advisers and 85 DFMs. Fieldwork was conducted between 7 June and 25 August 2021.

This article is provided for information only. The views of the author and any people quoted are their own and do not constitute financial advice. The content is not intended to be a personal recommendation to buy or sell any fund or trust, or to adopt a particular investment strategy. However, the knowledge that professional analysts have analysed a fund or trust in depth before assigning them a rating can be a valuable additional filter for anyone looking to make their own decisions.

Past performance is not a reliable guide to future returns. Market and exchange-rate movements may cause the value of investments to go down as well as up. Yields will fluctuate and so income from investments is variable and not guaranteed. You may not get back the amount originally invested. Tax treatment depends of your individual circumstances and may be subject to change in the future. If you are unsure about the suitability of any investment you should seek professional advice.

Whilst FundCalibre provides product information, guidance and fund research we cannot know which of these products or funds, if any, are suitable for your particular circumstances and must leave that judgement to you. Before you make any investment decision, make sure you’re comfortable and fully understand the risks. Further information can be found on Elite Rated funds by simply clicking on the name highlighted in the article.

Related insights

Will fixed income be the shining light of 2024?

Fixed income in 2024: what investors should expect

Which sector is poised for growth in 2024?