Is a quality growth approach required for 2023?

By Joss Murphy on 2 May 2023 in Equities, Global, Specialist investing

2023 had a notably volatile start to the year, as equity markets reacted to an increasingly uncertain and constantly changing macroeconomic backdrop. Here, Ian Mortimer and Matthew Page, co-managers of the Guinness Global Innovators fund, review the three stages markets experienced in the first quarter of 2023 and tell us why they continue to favour a quality approach to growth investing.

Stage 1: ‘Recovery Rally’

The year got off to a strong start as the sectors that performed weakest in 2022 rallied. Promising US inflation data spurred a bullish market outlook in which interest rates could come down sooner. The prospects for global economic growth seemed to be improving thanks to an improving European energy position (due to a warm winter and high storage levels) and China’s reopening. Equities were driven almost entirely by multiple expansion: a clear sign that investors were prepared to look beyond a weaker short-term outlook to the expected recovery in the second half of the year.

As illustrated in the chart above, the rally in January was led by the more cyclical areas of the market. Semiconductors, the Global Innovators fund’s largest industry overweight, was the second best performing industry and contributed strongly to returns over the period.

Stage 2: ‘The Market Reversal’

The market reversed course just three days into February as the positive sentiment that had driven equities quickly unwound. US and European employment and inflation data came in surprisingly ‘hot’, dampening the hopes of an earlier pivot away from tight monetary policy. The sudden market reversal pointed to the fragility of the prior rally.

A healthy US labour market had added 517k jobs, far exceeding the 185k consensus, and pushed the jobless rate to 3.4%, its lowest level in 53 years. Staff costs are the largest components of costs in the services sector. Services inflation, which tends to be particularly entrenched, has not yet peaked.

Compounding the negative sentiment, the Fed continued with its hawkish tone. Its chair Jerome Powell explained that there is still “a significant road ahead to get inflation down to 2%. If we continue to get strong labour market reports or higher inflation reports … we (may) have to raise more than is priced in.” This left little room for doubt about the Fed’s intentions.

As the chart below shows, over February, markets shifted their peak rate expectation from 4.9% in June 2023 to 5.4% in September 2023.

A noticeable rotation away from growth towards more defensive areas ensued. Value outperformed growth, but only by 0.9% in USD.

Stage 3. Banking Crisis and Fallout

The final part of the quarter was characterised by the banking crisis. It started eight days into March as fears around the liquidity of Silicon Valley Bank (SVB) gathered steam. SVB underwent a bank run and there was a detrimental loss of confidence in other regional banks (Signature Bank & Silvergate Bank defaulted), also causing troubles for international banks (notably Credit Suisse & Deutsche Bank).

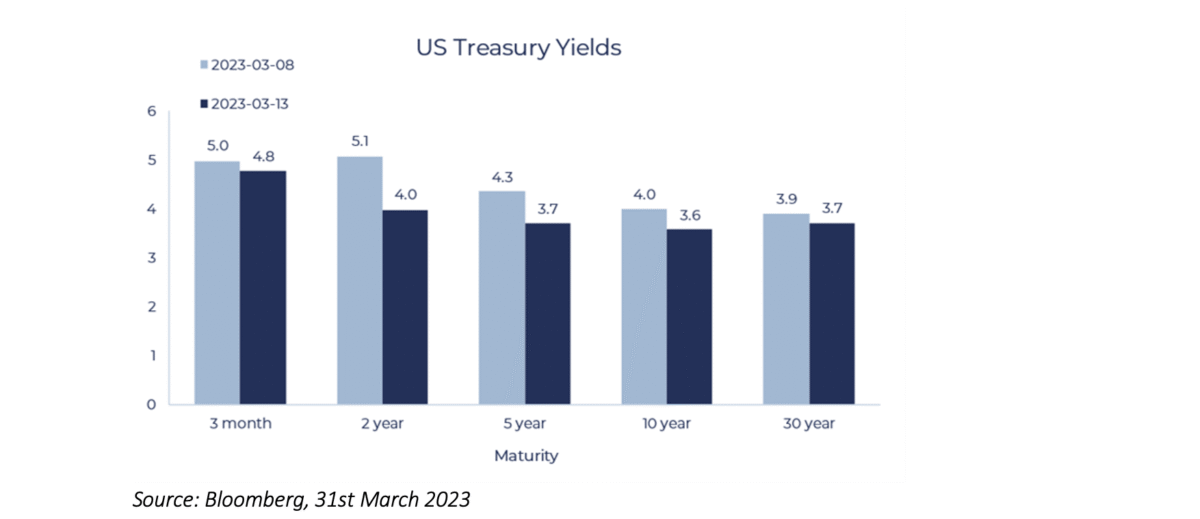

Money moved out of smaller banks towards the big four US names, which are deemed ‘too big to fail’. Alongside this, investors rushed to the relative safety of bonds, which caused prices to rise and yields to fall. The drop in US 2 Year Treasury yield was particularly sharp, contracting over 100bps (1%) in just five days. It is worth noting that the large inflow of funds into the larger US banks likely exacerbated this trend, as new deposit money was put to work.

Another consequence was de facto monetary tightening as banks made credit conditions stricter. History has shown that banking system weakness can have large and persistent effects on GDP growth.

Over this period, investors sought safety within large-caps and higher-quality businesses.

Further, quality growth businesses performed robustly as investors expected a more cautious near-term Fed policy (and thus the potential for lower interest rates in the case of further financial instability or an induced recession).

The Global Innovators strategy’s large-cap bias and focus on quality growth (over speculative or cyclical growth) were to its benefit in this period.

Where we are today

Putting banking issues to one side, equity investors must contend with numerous other problems, not least, the usual story of high inflation and interest rate uncertainty. At the latest policy meeting, the Fed raised rates 25bps (0.25%), a smaller increment than previously, but a clear signal that it remains focussed on bringing inflation under control despite domestic banking woes.

As the Fed stays the course with quantitative tightening, investors are looking at areas of market fragility which may give way next. This adds to volatility and has also led to a more pessimistic outlook at the company level, with earnings downgrades and lower GDP estimates weighing heavy on sentiment.

The combination of these headwinds means that we could well be in a lower-growth environment. This being so, we will be maintaining the Global Innovators strategy’s focus on quality growth – that is, businesses that can continue to grow in a low-growth environment thanks to structural demand drivers.

Photo by Artem Kniaz on Unsplash

This article is provided for information only. The views of the author and any people quoted are their own and do not constitute financial advice. The content is not intended to be a personal recommendation to buy or sell any fund or trust, or to adopt a particular investment strategy. However, the knowledge that professional analysts have analysed a fund or trust in depth before assigning them a rating can be a valuable additional filter for anyone looking to make their own decisions.

Past performance is not a reliable guide to future returns. Market and exchange-rate movements may cause the value of investments to go down as well as up. Yields will fluctuate and so income from investments is variable and not guaranteed. You may not get back the amount originally invested. Tax treatment depends of your individual circumstances and may be subject to change in the future. If you are unsure about the suitability of any investment you should seek professional advice.

Whilst FundCalibre provides product information, guidance and fund research we cannot know which of these products or funds, if any, are suitable for your particular circumstances and must leave that judgement to you. Before you make any investment decision, make sure you’re comfortable and fully understand the risks. Further information can be found on Elite Rated funds by simply clicking on the name highlighted in the article.

Related insights

Investing in a fractured world

Building your ISA portfolios by investor type

Building a low-maintenance ISA