Is it time to invest in social bonds?

By Sam Slator on 31 May 2021 in Sustainable investing

When it comes to ESG investing, much of the focus until now has been on the E and the G – the environment and governance. The social aspect has taken rather a back seat. But is all that about to change?

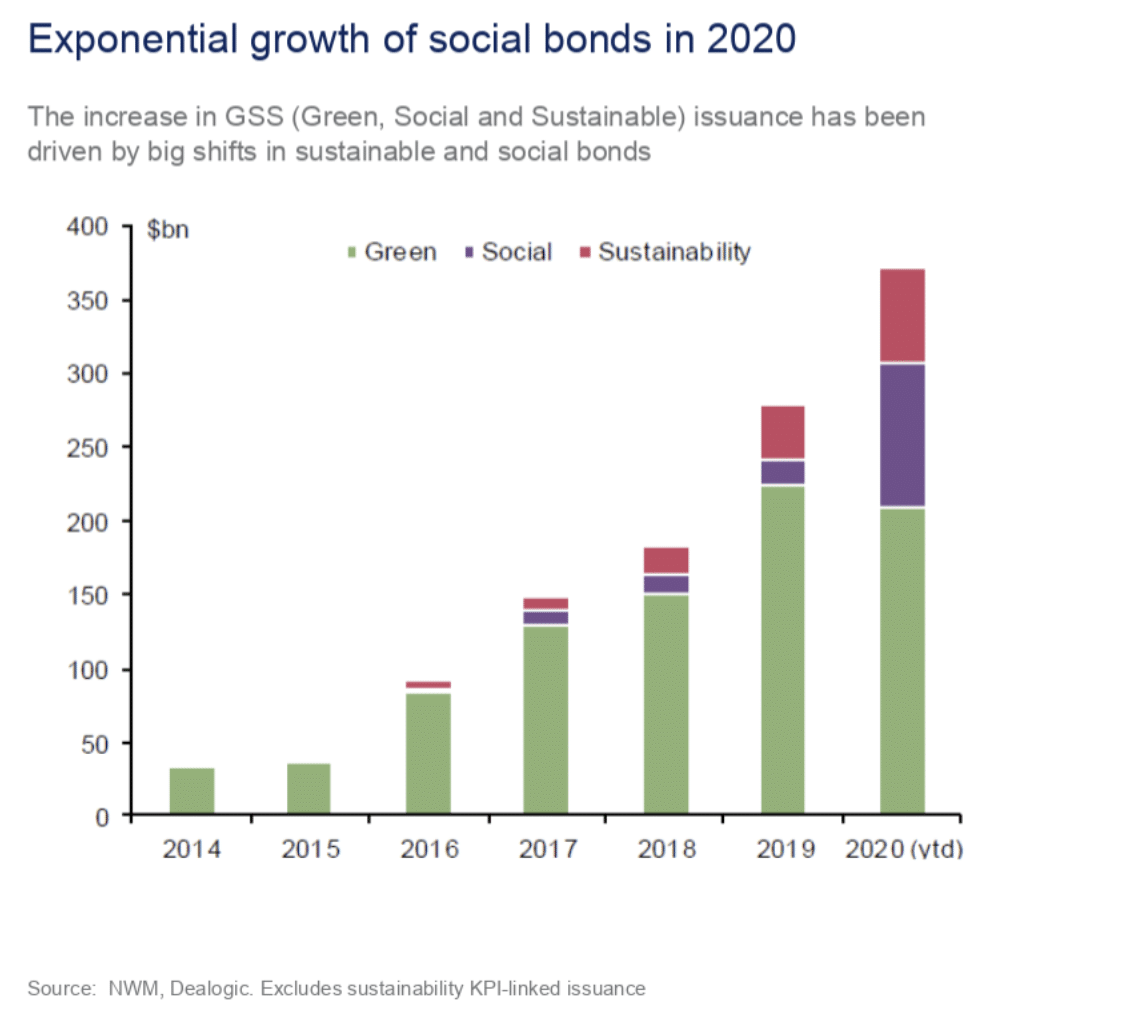

Global issuance of green, social and sustainability bonds is set to hit a record $650 billion in 2021, a 32%* increase over last year. And within that, social bond issuance increased seven-fold**.

What are social bonds?

A bond is like a loan – only it is companies and governments that issue bonds and investors who lend them the money. Social bonds are special bonds that fund a range of causes from access to education to affordable transportation and food supply protection.

According to Saida Eggerstedt, Schroders’ head of sustainable credit, the recovery from the global pandemic has been fuelling the expansion of social bonds “as governments across the world are looking to stimulate economies and create jobs while committing to ambitious environmental targets,” she said.

Mario Eisenegger, investment director of public fixed income at M&G Investments, commented: “Social bonds were the rising stars of a growing ESG bond market in 2020. In April 2020, Guatemala became the first country to issue a sovereign social bond aimed at financing COVID-19 response efforts.

“Corporate social bond issuance is also on the rise. With consumers now more attuned to social issues, social bonds provide companies with an instrument to demonstrate support for their wider stakeholders, from employees to customers and local communities.”

Katherine Kroll, senior sustainable investing specialist at Brown Advisory, tells us why social issues have been overlooked in the past, why it’s important that both society and investors think more about how company action can proliferate racism and environmental injustice, and why diversity and inclusion should be part of every investment process in this podcast:

What social bonds are available and who invests in them?

Despite the recent growth, social bonds still represent a fairly small part of the bond market and demand/supply dynamics can lead to tighter valuations compared to comparable bonds with a general use of proceeds. This means selectivity is key. And, so far, investment in social bonds is still very much the domain of specialist bond funds. Other, more mainstream, offerings are waiting for the market to develop.

“We’ve been investing in charity bonds for some time,” commented Bryn Jones, manager of Rathbone Ethical Bond fund. “More recently, we’ve invested in the Ford Foundation. It is challenging inequality and social injustice in the US and gender and ethnic issues world-wide working in the likes of Brazil and South Africa. Another example is the WK Kellogg Foundation, which has more of an educational focus, dealing with vulnerable children, families and communities and giving them a step up.

“During the pandemic, we also invested coronavirus response bonds. IFFIM is an example. It funds Gavi’s core immunisation programmes, which used to be more about irradicating polio and measles, but more recently it’s been helping the response to the coronavirus.”

There are also opportunities here in the UK – like the solar panel community farm in the West Country, that gives its excess revenues back to the local community for grants and education, or a wind turbine bond in the Scottish Highlands that puts its excess revenues back into the local community to create jobs and redevelop tourism.

“Traditionally, supranationals and governing bodies have been the main issuers in this market as they looked to raise funds for segments such as healthcare, employment and education,” commented Kenny Watson, co-manager of Liontrust Monthly Income Bond. “But we have also seen JP Morgan offer its inaugural social bond in recent months, designed to promote economic development by financing small businesses, affordable housing and projects promoting access to education and healthcare in low-moderate income areas.

“So far, the UK has lagged Europe in terms of issuance and what we have seen from charities and housing associations has typically been small and therefore illiquid. The social bond market is evolving in the UK, however, and there have been larger issues from housing associations such as Clarion Housing and Pearson more recently to fund educational learning.

“At present our funds have no exposure to social bonds, but if the market continues to evolve and the number of social bonds in issue increases, then, provided they meet our criteria, we would expect our exposure to increase over the next 12 to 18 months.”

Allianz Strategic Bond has no exposure either. Manager Mike Riddell said: “Social bonds are not an area that we focus on,” he said. “We are global macro top-down investors, and we invest across the main core areas. When we take credit/spread risk, which is where social bonds would potentially fit in, we very rarely buy many individual bonds, and generally prefer to take positions via indices. Our macro approach is all about getting the big picture global fixed income asset allocation decisions correct, where liquidity is always very important to us so that we change portfolio positions as our views evolve. Bottom- up research on generally illiquid social/project finance bonds are not really part of our investment remit.”

Johnathan Owen, part of team behind TwentyFour Corporate Bond fund, added: “None of our funds currently hold any social bonds but where their fundamentals and relative value appear favourable against other ESG related or conventional unlabelled bonds, we would have no underlying objection to holding them. Social bonds still make up a relatively small portion of overall ESG related issuance. However, this has increased significantly in the past year following pandemic related issuance, largely from governments and supranationals. Issuance from corporates remains very limited and will need to increase before social bonds are a common feature in bond portfolios like green bonds.

Jupiter’s fixed income team, which includes the manager of Jupiter Strategic Bond fund, are monitoring the asset class. “Social bonds are a fast-emerging sector of the bond market, but one that is still in its infancy,” they said. “However, given the rise in issuance seen in the green bond market over recent years then the expectation is that we will see social bonds take up an increasing portion of fixed income issuance, especially given the accelerated profile for ESG investments seen in 2021 so far.

“Good practice around ESG features is often, if not always, aligned with strong internal processes around all parts of any enterprise. The same analysis applies to the specific area around social bonds – any company that looks to benefit the local communities they operate in is very likely to have good practices in all facets of its day-to-day activities.”

*Source: Schroders, Moody’s Investor Service

**Source: Schroders, Bloomberg

This article is provided for information only. The views of the author and any people quoted are their own and do not constitute financial advice. The content is not intended to be a personal recommendation to buy or sell any fund or trust, or to adopt a particular investment strategy. However, the knowledge that professional analysts have analysed a fund or trust in depth before assigning them a rating can be a valuable additional filter for anyone looking to make their own decisions.

Past performance is not a reliable guide to future returns. Market and exchange-rate movements may cause the value of investments to go down as well as up. Yields will fluctuate and so income from investments is variable and not guaranteed. You may not get back the amount originally invested. Tax treatment depends of your individual circumstances and may be subject to change in the future. If you are unsure about the suitability of any investment you should seek professional advice.

Whilst FundCalibre provides product information, guidance and fund research we cannot know which of these products or funds, if any, are suitable for your particular circumstances and must leave that judgement to you. Before you make any investment decision, make sure you’re comfortable and fully understand the risks. Further information can be found on Elite Rated funds by simply clicking on the name highlighted in the article.

Related insights

What’s driving bond funds into 2026?

Debt, duration and discipline in bond markets

Ethical investment funds: a practical UK guide