A rare opportunity in high-quality European equities

By Chris Salih on 20 May 2026 in Investment Trusts

European equities outperformed expectations in 2025, reversing several years of relative underperformance versus the US, as a value rally, led by the likes of banks & financials and defence & industrials, saw the MSCI Europe return 26% across the calendar year* – comfortably the strongest in a decade.

A guide to Fidelity European Trust

The first quarter of 2026 saw similar optimism due to stronger earnings and improved sentiment. However, this changed in March with the onset of conflict in the Middle East – optimism has since given way to volatility and dispersion in returns, with inflation and rising interest rates back on the radar.

Fidelity European Trust (FEV) has had its challenges over the past couple of years. With a bottom-up portfolio and a focus on managing downside risk – the focus on quality growth has not been rewarded with rising bond yields, a headwind to the investment style. Other factors have also played a role – notably an underweight to German stocks; stock-specific challenges from the likes of Novo Nordisk; and a lack of exposure to peripheral banks like Santander and BBVA.

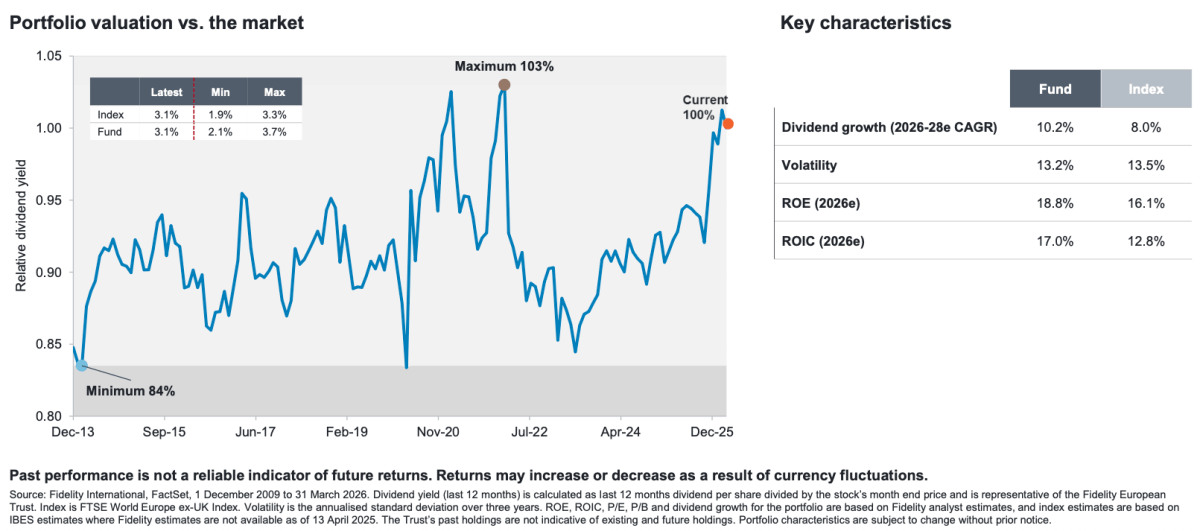

But there is a sense of optimism among the management that things are swinging back in their favour. The relative valuation of the portfolio is now at a very attractive level. Historically, FEV’s quality focus means it boasts a dividend yield that is between 5-15% more expensive than the market (both the index and FEV are currently trading on a yield of 3.1%)**.

That’s the view of Natalie Briggs, investment director on Fidelity European Trust. Natalie says the fact the portfolio is now trading on a similar dividend yield to the market is “historically a very good buy signal”.

FEV is a core European equity portfolio with a disciplined and cautious long-term focus. Although not an income fund, the team wants companies which can sustainably grow their dividends over time. Managed by Sam Morse and Marcel Stötzel, the trust looks to outperform its benchmark by 1-2% per annum post fees. Despite a challenging 2025, long-term performance has been excellent, producing an annual return of 9.8% per annum since Sam took over the portfolio in 2011**.

FEV completed a merger with Henderson European Trust in 2025 to create the largest European equity trust in the sector.

Investment Process

FEV’s investment philosophy is broken down into three core principles:

- Bottom-up – whereby there is a stock-selection focus.

- Long term – as the team believes long-term thinking reduces costs and improves performance.

- Cautious – with a focus on managing downside risk.

Although this is not an income fund, the dividend forms a core part of the fund’s philosophy. In particular, there is a heavy emphasis on dividend growth. This is because the team believes there is clear evidence that companies which consistently grow their dividend over time outperform.

A big priority for the fund is preserving client capital relative to the benchmark. Idea generation comes from Fidelity’s European research analysts. Sam and Marcel can also make use of external sources such as company meetings or external analysts and experts.

Potential ideas are initially assessed from four perspectives. The first is positive fundamentals – looking for structural growth, good return on capital and dividend growth prospects; the second is the ability to generate cash; the third is a strong balance sheet, as the managers dislike highly levered companies; and the fourth is an attractive valuation – looking for good quality at a reasonable price.

Sam and Marcel will then meet the company to reinforce conviction in the four areas above. They want companies which can grow their dividends sustainably for at least the next 3 to 5 years. The team then applies Sam’s ‘three good reasons to buy a company’, which include two fundamental reasons combined with one valuation reason. If a company passes all these stages and the ‘three reason test’, they will initiate a position.

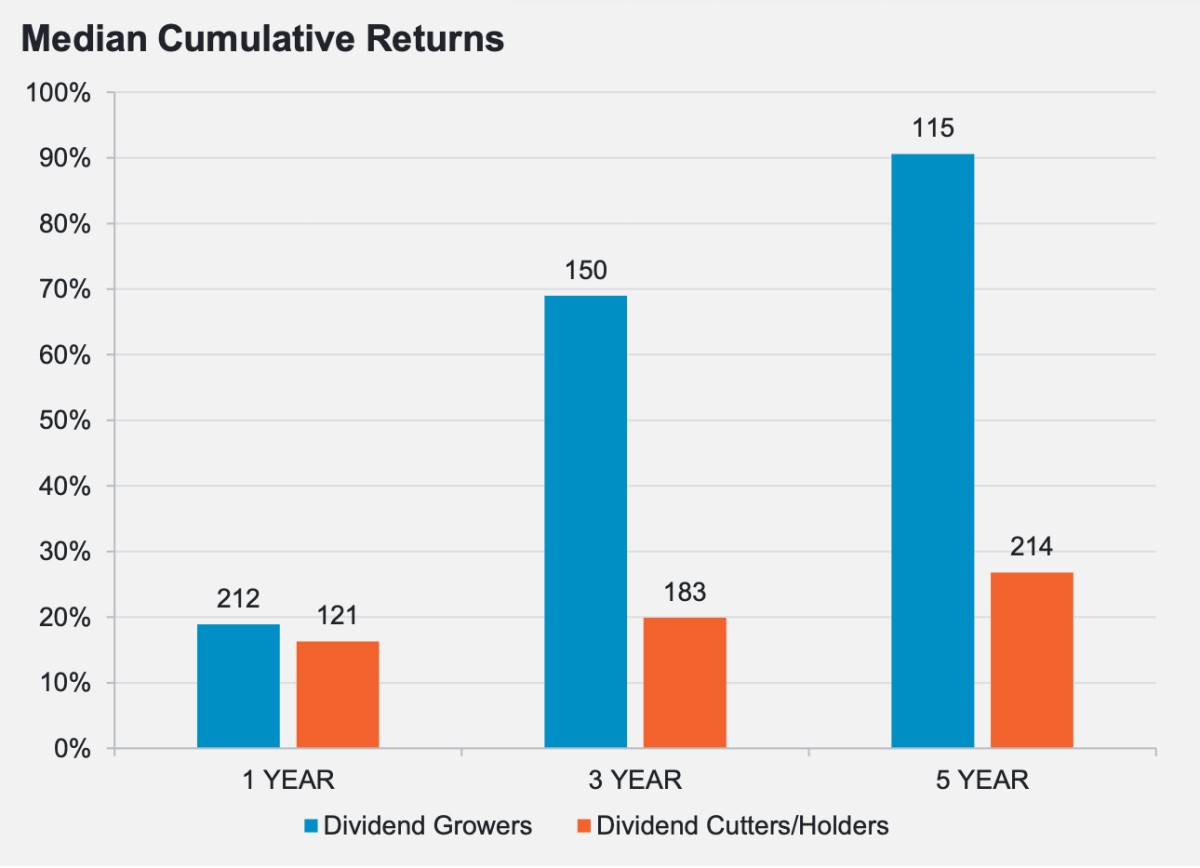

For clarity, the chart below shows 115 European companies which have raised dividends consistently over the past five years**. It is not a case of just using those names in the portfolio as they change constantly; it is about finding those with strong positions to maintain dividend growth and those new names likely to join the list. Those that have consistently grown their dividends have significantly outperformed their peers**.

The portfolio is then constantly reviewed and if any of the three reasons change, this prompts a review of the stock. The final portfolio will hold 45-60 stocks.

Why now for this portfolio?

- Excellent long-term track record with FEV producing a 212% share price return over the past decade (149% for AIC Europe sector)***.

- Unusually attractive entry point with FEV’s dividend yield (3.1%) the same as the index – it has traditionally been on a 5-15% premium.

- Growing caution and rising volatility caused by what is happening in the Middle East may suit a core portfolio focused on quality businesses.

- Focus on companies growing dividends has proven to be a successful guide to performance

- Fees have been reduced following the merger with Henderson European Trust in September 2025 (0.68%).

Manager’s View

Natalie says the management team are mildly bearish at the moment because European earnings and dividends are expected to jump from almost no growth in 2025 to double-digit growth in 2026-2027, as people expect the cyclical recovery to start coming through in industrials and other parts of the market.

She says they have started to see that in some of the industrial numbers coming through in the early part of the year, but the war in the Middle East means that recovery is likely to be pushed out a little further, particularly in Europe where we are very energy price dependent.

The worry is that this impacts inflation and consumers start to feel the pinch on both bills and petrol prices. This is all at a time when sentiment has been positive and valuations are reasonably high across a number of sectors.

“The Middle East situation changes everything in the short term. If we get a resolution there (as well as the Ukraine), the focus will shift to things like fiscal spending, with budgets allocated to building and rebuilding.”

She says we have already seen some of the levers pulled in terms of Europe’s improving outlook – citing Germany’s fiscal debt break and Europe’s increased defence spending. Resolution to these conflicts could see improvements in other areas, like improving regulation and greater coordination and integration – prompting European consumers to tap into their large savings rates.

Performance challenges: why the managers are confident of a turnaround

The managers have acknowledged they have not outperformed since the start of 2025 for a number of reasons. In 2025, FEV produced an NAV total return of 16.2%, compared with 27.9% for the FTSE Europe ex-UK index. This has continued thus far in 2026 (FEV NAV return of -1.1% vs. 2.8% for the index)**.

Analysis of the NAV total return places stock selection as the biggest detractor (-13.2%). This is for a few reasons, notably some stock-specific challenges for the likes of Novo Nordisk, Symrise, Partners Group and 3i Group**.

Danish pharmaceutical business and index heavyweight Novo Nordisk, best known for its Wegovy weight-loss drug, has faced a challenging period over the past year or so. The team recently sold out of the position following the CagriSema Obesity trial failure in February 2026, which followed on from the failure of its Alzheimer’s trials late last year.

Natalie says they have turned bearish on the firm despite the successful launch of the oral version of Wegovy, citing that it will cannibalise existing injectable sales. There will be further pressure when Eli Lilly launches its own oral version.

Another example is specialist chemicals, flavours & fragrancies provider Symrise. Natalie says while Symrise’s manufacturing and development capabilities are complex and difficult to reproduce, they have started to sell down in April 2026, triggered by the impact of war in the Middle East – highlighting high energy costs, supply chain disruptions, and cautious consumer spending.

A big priority for the fund is preserving client capital relative to the benchmark. This is done in three ways. Firstly, FEV will typically have a beta of less than one on an unlevered basis (this can go above one due to gearing); secondly, the trust has sector guardrails (sector weights risk controlled within +/- 5% of the index) which helps them deal with left-field events such as Covid and Russia’s invasion of Ukraine; thirdly, the managers and analysts all spend additional time reviewing downside protection on every stock they hold.

The guardrails can see FEV underperform when certain countries or sectors dominate returns – as was the case in 2025. For example, they were underweight Germany amid the fiscal expansion; a boom in industrial and defence stocks; and strong earnings from globally-exposed German companies. Natalie says the underweight has been cut from -5 to -2% from the benchmark. She says:

Other headwinds included defence holdings. US vice president JD Vance spoke at the Munich Security Conference in February 2025, where he sharply criticised European governments and also pushed the idea that Europe needed to take more responsibility for its own security and defense. It was seen as a catalyst for European countries to be less reliant on the US and increase their own defence spending. FEV has some exposure through the likes of MTU Aero Engines, but the managers say many defence stocks do not meet their criteria on the likes of dividend and cash conversion – and that while some of this has changed, many are now quite expensive relative to their own history.

Financials have also been a headwind, with underweights to peripheral banks like Santander, UniCredit and BBVA – it should be noted FEV does have a number of banks which have contributed to performance (Bankinter, ABN Amro, KBC Group and Intesa Sanpaolo were the top four contributors in 2025.)

However, arguably the biggest headwind would be style, as quality and growth have been left behind amid this value rally. FEV’s focus is strong balance sheets and dividend growth, which has struggled as the market has chased defence and infrastructure names as well as cyclical companies.

FEV has a diversified exposure to AI as a theme throughout the portfolio – this ranges from “picks and shovels” holdings like Legrand, a global specialist in electrical and digital building infrastructures, and Schneider Electric. Natalie says the latter has two-thirds of its revenues exposed to depressed industrial and construction markets – meaning there is limited downside risk.

ASML remains a core holding in the portfolio, given its monopoly in semiconductor lithography equipment, an essential part of all semiconductor manufacturing,

Natalie says some of the losers they have had in the AI space have been unfairly punished. An example of this is technology consulting business SAP, which they feel has the ability to defend against AI, with many of its products already embedded in businesses. SAP is also using new AI tools to bolster its business proposition.

Reaction to change and renewed optimism

The team have made some changes to the portfolio given their cautious outlook and response to a challenging period.

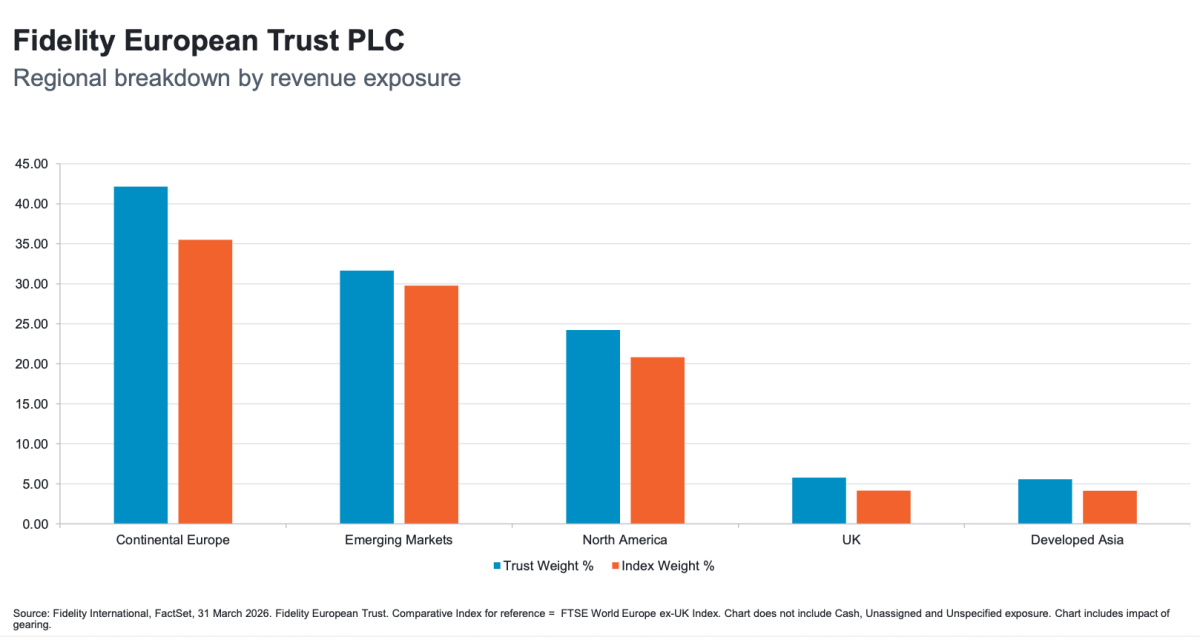

The biggest overweight currently is continental Europe – the team have been looking for stocks with more domestic European revenue exposure. These companies are still looking to build a global footprint. Inditex, for example, has 70% of its revenues coming from Spain, but lots of growth Europe-wide and is growing into the US.

They have also been adding to their banking names – with a preference for regional names with strong domestic positions. Examples include AIB Group, Nordea Bank and BNP Paribas (all of which they believe are well positioned for the recovery of domestic European spending if we see a resolution to the aforementioned geopolitical concerns).

Natalie cites BNP Paribas as an example of a bank which is likely to benefit from rate rises over the longer term. She says: “Some of the peripheral European banks like Santander, BBVA – which we did not own – did really well through last year and we missed that because some of the earnings growth was much faster than some of the other banks. This is because as soon as rates rose they were able to increase the rates they charge to mortgage customers and a bit slow to pay their depositors the extra interest on the other side.

“BNP has many customers on fixed rate mortgages – so there is a lag effect. There is a big book of business for the likes of BNP in the next few years – they still have those benefits to come through, unlike the peripheral banks.”

“You can have your cake and eat it too”

Natalie says this an interesting point for the trust given the dividend yield (3.1%) is the same as the index. The trust typically trades at a premium to the market because of the stronger dividend growth, lower volatility, return on equity and return on invested capital metrics.

“We think it is a good time to buy on a relative basis to the market – particularly as it tends to do well in a risk-off environment. We usually trade at a 5-15% premium on dividend yield to the market. FEV is almost looking as cheap as it has ever been, but the fundamentals and characteristics of the portfolios still look strong. Better dividend growth, lower volatility than the market, greater ROE and ROIC,” she says.

Natalie also says FEV is in a strong position regardless of the direction of markets from this point. Should bond yields rise, the defensive qualities of the portfolio will kick in, while a fall in bond yields should be offset by the growth bias in the trust.

Performance

As mentioned, the trust has produced an annual return of 9.8% per annum since Sam Morse took over as manager on 1 January 2011 (vs. 8.8% for the index). Over the past 10 years, FEV has returned 212% on a share price total return perspective (149.1% for the IT Europe sector) – while FEV has an NAV total return of 194.8% (vs. 142.9% for the sector)**.

What else do investors need to know?

- Gearing: Gearing tends to be in the 10-15% range – it is currently at the lower end due to their caution on markets. FEV is mainly geared using derivatives, using a mixture of index futures and CFDs. As part of the merger with Henderson European (HET), FEV took on a small amount of long-term debt, which was issued at very low interest rates. The total stands at €35m.

- Dividends: Although there is no specific dividend target, FEV has a consistent track record of dividend growth, as the managers believe it is a key signal that company management cares about shareholders and the long-term future of their business.

- Discount: The discount currently stands at 5.1% (6% average discount over the past five years)****. The Board introduced an enhanced discount policy with the aim of maintaining any share price discount to NAV in mid-single digits (previously 10%).

- Charges: The management fee payable by the Company will be reduced to a tiered structure: 0.70% up to 400m, 0.65% from 400m to 1.4bn, and 0.55% above 1.4bn***.

Outlook

Natalie says the team are encouraged that the portfolio is trading on a similar dividend yield to the market. After a challenging 2025, she says the focus is on improving execution – historically the trust has faced style headwinds before (2022) and strong stock selection has helped them, something which did not happen in 2025.

Nevertheless, long-term history shows the team are very adept at finding those companies which can grow their dividend sustainably. The 115 companies that have done so over the past five years have significantly outperformed their peers – so there is no reason to suggest why this cannot continue.

The managers are also able to leverage off the huge resource at Fidelity, including 135 analysts globally – this is important given two-thirds of the revenues of European-domiciled companies come from outside Europe.

We believe the team’s core approach, coupled with attractive dividend yield, makes this an attractive option for investors at a time when uncertainty over the economic outlook continues to grow.

*Source: FE Analytics, discrete calendar year performance in pounds sterling of MSCI Europe, 2016 to 2026

**Source: Fidelity European Trust PLC, March 2026

***Source: AIC, 15 Mary 2026

****Source: FE fundinfo, 15 March 2026

This article is provided for information only. The views of the author and any people quoted are their own and do not constitute financial advice. The content is not intended to be a personal recommendation to buy or sell any fund or trust, or to adopt a particular investment strategy. However, the knowledge that professional analysts have analysed a fund or trust in depth before assigning them a rating can be a valuable additional filter for anyone looking to make their own decisions.

Past performance is not a reliable guide to future returns. Market and exchange-rate movements may cause the value of investments to go down as well as up. Yields will fluctuate and so income from investments is variable and not guaranteed. You may not get back the amount originally invested. Tax treatment depends of your individual circumstances and may be subject to change in the future. If you are unsure about the suitability of any investment you should seek professional advice.

Whilst FundCalibre provides product information, guidance and fund research we cannot know which of these products or funds, if any, are suitable for your particular circumstances and must leave that judgement to you. Before you make any investment decision, make sure you’re comfortable and fully understand the risks. Further information can be found on Elite Rated funds by simply clicking on the name highlighted in the article.

Related insights

Why Europe offers security for an uncertain investor

Balancing growth and income for long-term returns

Is the great British pub still worth investing in?