“We are well positioned for a period of stagflation – and we believe there is a strong chance that we are entering this soon. If you go back to the stagflationary period seen in the 1970s – conventional bonds and equities really struggled. Energy producers did well, as did gold, and so would index linked bonds if they had existed. Cash also delivered a positive return – and we’ve got lots of cash-related instruments now. All of this is so we can help investors sleep at night.”

The Eeyore of investment trusts that consistently delivers

By Chris Salih on 21 April 2026 in Investment Trusts

Please note, this interview took place on 3 April 3 2026, during the height of market uncertainty following the announcement of the US war with Iran and all views are as of this date

This year marks the 100th anniversary of the release of a book covering one of the world’s most popular children’s characters: Winnie-the-Pooh. Written by A.A Milne and set in Hundred Acre Wood, the short stories covered the adventures of the teddy bear and his many friends including Christopher Robin, Piglet, Owl, Rabbit, Kanga & Roo.

But the one friend that sticks out for many readers is Eeyore – the pessimistic donkey, who often worries about his tail falling off or things going sour generally. But he is also both wise and a realist, who accepts bad things can happen and is ready to manage the consequences – whereas others may be in denial.

There are plenty of investors who have a similar approach; while some bounce through markets with the optimism of Tigger, others have a more subdued approach – and focus on what could go wrong. Bull markets reward confidence, not caution. But when conditions turn, as they have done recently, it’s often the “Eeyores” who are still standing as they realise markets are cyclical, losses can hurt more than gains help and avoiding drawdowns matters more than chasing every rally.

Capital Gearing Trust (CGT) has a touch of the Eeyore’s in its own investment approach. Launched in 1982, it aims to preserve investors’ real wealth over time and deliver returns ahead of inflation, rather than simply chasing short-term performance or beating a specific market benchmark. The managers do this by investing across a range of holdings including equities, bonds, investment trusts, ETFs and cash.

says Chris Clothier, who co-manages the portfolio alongside Peter Spiller and Alastair Lang. Spiller founded Capital Gearing Asset Management (CGAM) in 2000 and has actually managed this trust since its launch back in 1982.

Investment Process

CGT’s investment objective is to generate returns ahead of inflation, without losing money. The trust looks to achieve these returns over the long term through a global portfolio of equities, bonds and commodities offering both diversification and risk management.

The investment process sees assets placed in three core buckets.

- The first bucket is risk assets, which includes the likes of equities/funds, property and infrastructure.

- The second bucket is inflation-linked bonds – this is because they have a negative correlation to equities and typically outperform conventional government bonds. This includes the likes of US TIPS, UK Linkers and other high-quality sovereigns.

- The remainder will go into the third bucket – this is the managed liquidity reserve, which includes cash & treasury bills, short-dated government bonds and short-dated credit. This bucket also looks to reduce the duration and volatility of the portfolio.

Duration, currency and liquidity are all actively managed within the portfolio. The final portfolio is typically quite diverse with between 175-200 holdings. With an ongoing charge of 0.56%*, the trust is also very cost efficient.

The focus on capital preservation and inflation-adjusted growth has seen the trust produce a positive return in 41 of the past 43 years, and has returned 64.6% to investors over the past decade**. CGT has also demonstrated an ability to defend capital in challenging periods, such as Covid and Liberation Day in 2020 and 2025 respectively.

Why now for this portfolio

- Excellent long-term returns – positive return in 41 of the past 43 financial years

- Ideal for challenging periods in markets (historically it has protected well on the downside)

- CGAM founder Peter Spiller has managed CGT since launch in 1982 in a variety of different conditions

- A strong defence against inflation eating into financial returns

- Ongoing charge of 0.56%* is attractive

- CGT operates a strict discount control mechanism, in place since 2015, to keep the share price trading close to its NAV, typically within a narrow range (around 2% premium or discount)*

Manager’s View

Clothier says when events like the US and Israel’s war with Iran come along, it is not simply a case of switching from an offensive to defensive footing within a portfolio – with the aim being to be positioned ahead of time to withstand shocks to the economy. A recent example came around ‘Liberation Day’ in 2025, when global equities (MSCI World) experienced a 18% peak to trough decline over the broader run-up and aftermath of the event, compared with just 2% for CGT***.

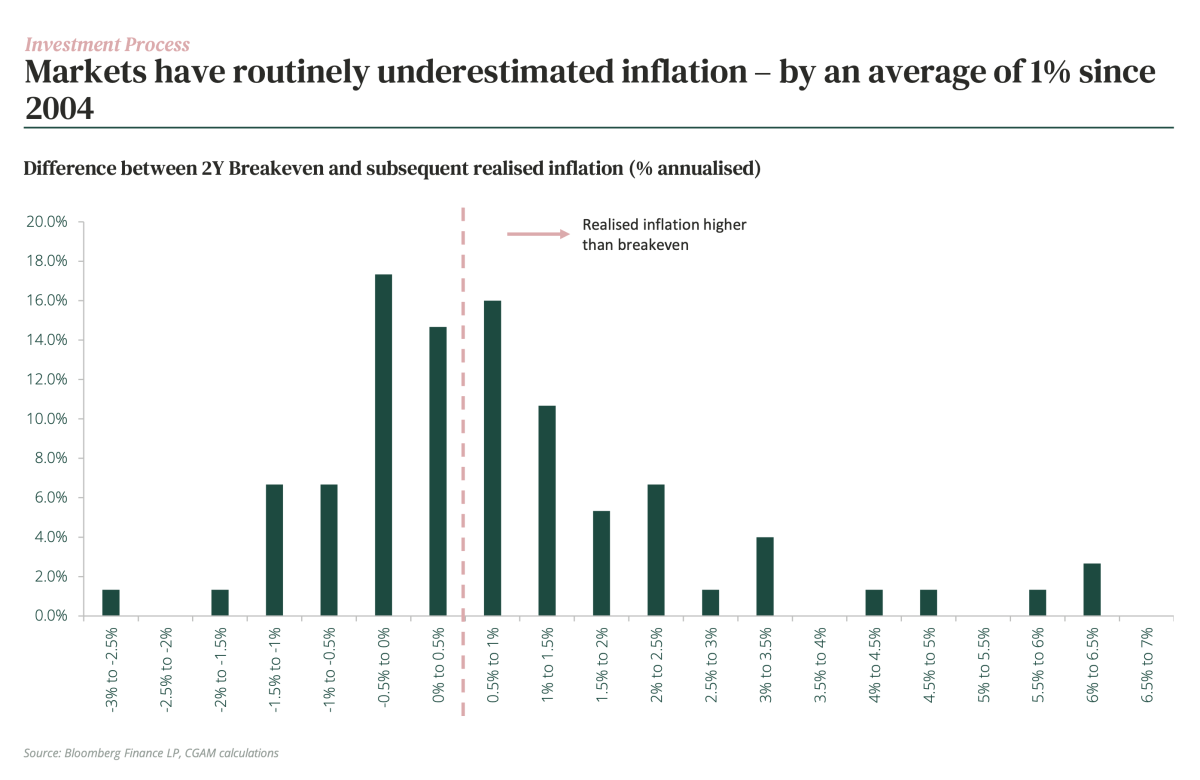

Inflation is the bogeyman for markets and it is certainly front and centre of CGT’s thoughts. A simple calculation shows that £100 in 2016 would have lost approximately 29% of its purchasing power by April 2026, meaning it would require about £141.45 today to match the same buying power due to the impact of inflation. Clothier says:

“Inflation tends to be the single biggest threat to investors’ wealth. If you look at the 1970s it was a disaster for most asset classes, if you go back to WW2 – every single inflationary event since that period has come about either because of war or an oil price shock – and quite often both things are correlated. War and energy prices increase inflation and that tends to be bad for both bonds and equities.”

CGT had already moved to a more defensive footing in late 2025, with the risk bucket within the portfolio reduced to 23% (included a near all-time low of 15% in equities), while holdings of UK inflation-linked bonds were increased.

Clothier says the team felt there were two radically different paths this war could take. The first of these being that US President Donald Trump could simply declare victory and “walk off the pitch”, the other being that he gets more aggressive and moves military assets into the region. Clothier says there is currently no clear indication on what path he will take.

He says: “If he does walk off the pitch declaring victory – then what does that mean for energy prices? Will they fall? If you look at the price of Brent Oil today vs 12-month Brent – the difference between those two is essentially at record levels (the spread is close to $40 a barrel 12 months vs spot). The market is saying this will get resolved within a year and we’re not going to bet against the market – but there is a pretty reasonable chance it doesn’t.”

He continues to add that even if Trump does declare victory, Israel may continue to wage war on Iran’s proxies in the region; meanwhile the concessions Iran has been asking for – such as guarantees of no future strikes and reparations – will not be forthcoming.

Beyond geopolitics: What’s keeping the managers awake at night?

The nature of CGT indicates the management team are typically cautious – and today is no different.

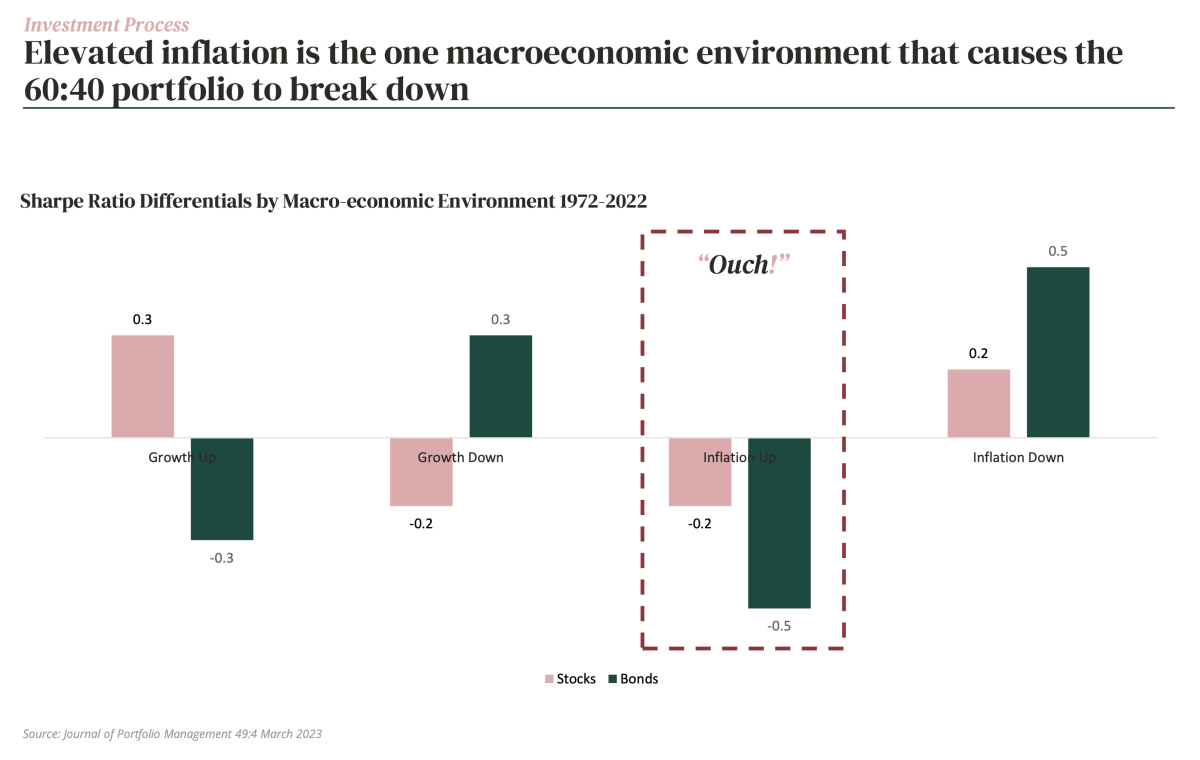

The main concern which stands out is the ongoing threat of inflation. Prior to the issues with the US and Iran, the team noted continued bullish forecasts for equity markets – all of which are anchored to the idea of falling rates and infrastructure investment. The epicentre of this worry is that while equity markets look expensive, bond markets look fragile because of huge government deficits. The fiscal deficits of most economies have grown since Covid as many spent money they simply did not have. All of this points to inflation running at higher-than-expected levels for a prolonged period – and CGT says elevated inflation is one of the macroeconomic environments that causes the 60/40 portfolio to break down.

The managers also believe equity market valuations appear stretched, citing that by market-cap, a third of the S&P 500 is trading at more than 10x revenues.

“Our concerns about valuations in the S&P 500 are less about the Magnificent Seven and more about the 493 other companies in the S&P 500, which we think are expensive,” Clothier says.

The team are also wary that the business models of the mega-cap, AI-related businesses are becoming more capital intensive. In its view, the returns on investment required to justify the planned levels of capex may be difficult to achieve. Clothier says if they thought these companies were attractive, it would not matter whether we were in an inflationary or deflationary environment – he says the likes of NVIDIA do look expensive, while semiconductors have historically been a cyclical business and it would be “a brave person who bets against that on this occasion.

He says: “The likes of Microsoft and Google – those are incredibly high-quality businesses with fantastic franchises and earnings profiles. Our concern about them is that it looks like over the next five years the hyper-scalers are going to spend $3 trillion in CapEx and that would require B2B revenues of $3-4 trillion to generate a decent return on those investments.”

Clothier says they are also concerned that the rate rises seen in recent years have not yet fully flowed into the property market – making them cautious here as well. They are also wary of the behaviour of gold, having sold their entire holding at over $5,000 an ounce earlier this year. Once considered a store of wealth – the team believe the yellow metal is now behaving like a risk asset.

Portfolio positioning and changes

There have been very few changes made to the portfolio in recent months. In December 2025, the team reduced the duration of their inflation-linked bonds as they did not see an imminent recession, especially as the US economy was being strongly stimulated by the administration.

Clothier says the protected nature of long-term bonds seemed less valuable; on the flip side of the large stimulus was the rising probability of a bond market crisis, therefore pushing them towards shorter-duration assets.

Bucket One – Risk asset (23% of the portfolio)

Clothier says that at just shy of 15%, the equities allocation within the portfolio is about as low as it gets and has been this way for the past six months – adding that equity prices have not changed meaningfully since the war started.

Valuations are also stretched, with the cyclically-adjusted PE ratio at about 40x in the US. According to the Cape ratio, Clothier says US equities have only been more expensive for 1% of US history.

We’ve discussed the concerns around property and gold above, but the team are also less focused on renewables than they were previously. When the prices of many of these trusts increased over the summer, the team sold down positions; exiting holdings in The Renewables Infrastructure Group (TRIG), Greencoat UK Wind and Foresight Solar, and reducing the holding in Bluefield Solar Income Fund.

However, they do have a 5-6% position in core infrastructure – with names like HICL, International Public Partnership (INPP) and 3i infrastructure. It should be noted that the management group behind Capital Gearing Trust successfully led a shareholder revolt against HICL, forcing the company to abandon a proposed £5.3 billion merger with The Renewables Infrastructure Group (TRIG), citing the appalling value and the benefits leaning towards shareholders of TRIG over HICL.

Bucket Two – Inflation-linked bonds (45% of the portfolio)

This is the bedrock of the portfolio, with CGT currently evenly split between both inflation-linked bonds and TIPs.

Clothier says the duration of inflation-linked bonds is currently five years (it was seven years), with the reduction reflecting their concerns over government fiscal deficits and the growing potential of a bond market crisis. Clothier says that CGT’s current asset allocation reflects a cautious stance relative to other multi-asset investment trusts.

Bucket Three – Managed Liquidity (32% of the portfolio)

Clothier says this bucket is also close to all-time highs for two reasons. The first of these is that even though their inflation-linked bonds are relatively short duration, if you are nervous about bond markets generally, then you want to have a reasonable pot that is close to cash. The second is that they have a relatively low duration across this bucket of just 1.5 years. He says

“We’ve been buying a UK 2-year bond and a slug of 12-18 months Japanese government bonds hedged back to sterling, where we get extra returns. We have 12% in credit, spread 50/50 between inflation-linked corporate bonds (4.5 years duration) and that is balanced with very short duration, nominal investment grade credit, typically with duration of less than a year.”

Performance: consistency over the long term

At the centre of the three investment pillars mentioned above is an absolute return mindset and that is supported by CGT producing positive returns in 41 out of 43 financial years (figures to 31 March 2025). The last of the two outliers came in 2023, as surging interest rates hit performance – particularly within the property allocation – resulting in the share price moving from a small premium to a small discount.

CGT has comfortably outperformed inflation over the past decade (64.6% vs. 39.8% for the Consumer Prices Index)**, having only underperformed in two calendar years in that period (2022 and 2023) when inflation was spiking in markets.

The NAV of the trust has risen 69% over the past decade*.

Recent success for the portfolio has come from risk assets – with strong performance from their holding in the BlackRock Energy Resources Income fund and their emerging markets and Asia Pacific holdings.

What else do investors need to know?

- Gearing: CGT generally employs a low or no structural gearing strategy, focusing on capital preservation rather than aggressive leveraging. As of April 2026, the trust reports very low or minimal net gearing, frequently operating with a “dry powder” approach that holds high levels of cash and short-duration assets.

- Discount: CGT has operated a strict discount control mechanism since 2015 to keep the share price trading close to its NAV, typically within a narrow range (around 2% premium or discount). The discount spiked in 2023–2024 primarily due to a temporary breakdown in its share buyback mechanism, coupled with a general, market-wide sell-off of investment trusts caused by rising interest rates and changed cost disclosure rules. This was resolved in early 2024.

- Dividends: The company pays a single annual dividend but focuses on total return rather than any net income level (102p per share at 31 March 2025)^.

- Fees: Ongoing charges are attractive at 0.56%*. The investment manager CG Asset Management Limited received an annual management fee equal to 0.60% of the net assets of the Company up to £120 million, 0.45% on net assets above £120million to £500 million and 0.30% thereafter, based on quarterly valuations and payable quarterly in arrears*.

Outlook

As Chris Clothier mentions, there is a wide range of outcomes to the Iran war at this stage, but history shows that it brings inflation and inflation shocks can take a very long time to pass through the financial system, particularly with a number of inflationary actions already in play in markets (Trump’s protectionism and government fiscal deficits across the globe).

Equity valuations appear resilient and still look expensive, but the bond market senses danger, as highlighted by the steepening US Nominal Yield Curve spreads. CGT is ideally positioned to offer investors peace of mind in this environment by taking away concerns about conventional bonds and equities falling together by focusing on the likes of inflation-linked bonds and US Tips to protect downside losses.

We like the use of its flexible investment asset allocation strategy as a way of navigating risk whilst demonstrating an ability to deliver growth over the long term. All of which has been demonstrated by good performance across the past four decades.

*Source: AIC, 17 April 2026

**Source: FE Analytics, total returns in pounds sterling, 15 April 2016 to 17 April 2026

***Source: FE Analytics, total returns in pounds sterling, 19 February 2025 to 8 April 2025

^Source: annual report, 31 March 2026

This article is provided for information only. The views of the author and any people quoted are their own and do not constitute financial advice. The content is not intended to be a personal recommendation to buy or sell any fund or trust, or to adopt a particular investment strategy. However, the knowledge that professional analysts have analysed a fund or trust in depth before assigning them a rating can be a valuable additional filter for anyone looking to make their own decisions.

Past performance is not a reliable guide to future returns. Market and exchange-rate movements may cause the value of investments to go down as well as up. Yields will fluctuate and so income from investments is variable and not guaranteed. You may not get back the amount originally invested. Tax treatment depends of your individual circumstances and may be subject to change in the future. If you are unsure about the suitability of any investment you should seek professional advice.

Whilst FundCalibre provides product information, guidance and fund research we cannot know which of these products or funds, if any, are suitable for your particular circumstances and must leave that judgement to you. Before you make any investment decision, make sure you’re comfortable and fully understand the risks. Further information can be found on Elite Rated funds by simply clicking on the name highlighted in the article.

Related insights

Five last-minute ISAs for the anxious investor

5 new funds gain an Elite Rating this Valentine’s Day