What is the key to a UK small-cap revival?

By Chris Salih on 17 February 2026 in UK

Battered, bruised and beaten – UK smaller companies have been in the doldrums for a decade now, having significantly underperformed their large-cap peers in the FTSE 100.

However, for many managers this weakness has created compelling opportunities – and we are starting to see some change as a result. M&A has been prominent for the past couple of years, while many smaller companies have started to recognise their own value and embark on share buybacks.

But while some investors have seen the opportunity, the dial has yet to shift on valuations. Some would argue this is simply a result of pension funds divesting in UK plc. We’ve seen exposure fall from 50% to closer to 2-4% as investors sought further diversification (global funds), while many defined benefit schemes de-risked by moving equities to bonds.

However, there are hundreds of burgeoning UK businesses, with all the fundamentals in place to grow. So, what can change sentiment and create an inflection point for these companies?

That’s the view of Georgina Brittain, manager of the JPMorgan UK Small Cap Growth & Income Trust (JUGI). The trust aims to provide investors with capital growth and an enhanced dividend from UK-listed companies further down the market-cap scale. It invests in high-quality, fast-growing, and innovative smaller companies that drive the UK economy, using a bottom-up approach to identify attractive stocks.

Georgina has worked at JPMorgan since 1995 and has been named manager on JUGI since 1998 (having managed its predecessor JPMorgan UK Smaller Companies). She is joined on the portfolio by Ketan Patel.

Investment Process

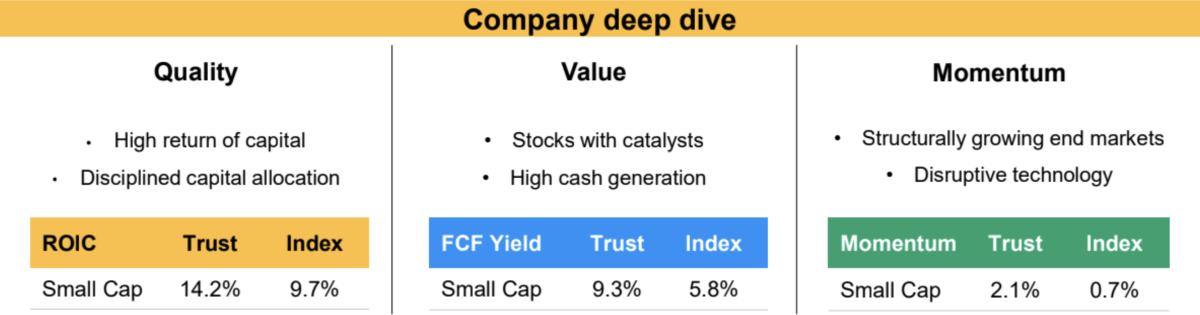

The team’s ethos is that attractively-valued, high-quality stocks with positive momentum outperform the market. To find these companies, the team essentially want to answer three questions:

- Is it a good business?

- Is it attractively valued?

- And is the outlook improving?

Stocks must be profitable and cash flow generative to be considered for inclusion. The quality of the business is evaluated through the profitability, sustainability of earnings and capital allocation discipline, while the company valuation is assessed to see if its prospects have been incorrectly estimated by the market.

The final element (is the outlook improving) looks at the operational momentum of the business and how this is being reflected in expectations. The firm’s VQM Model (Value, Quality, Momentum) screens stocks across all three factors and gives each a final score from 0 to 100 (0 is the best and 100 the worst). It should be noted that this is just a guide and not the sole source of buy and sell decisions.

The final portfolio holds between 60-120 holdings. The trust can, and does, hold a meaningful allocation to medium-sized companies. The team will tend to build into positions – for example, they will hold a small position in a company following its IPO and will add as they prove themselves.

Prior to the merger, the trust did not have a specific income target. However, following the merger with JPMorgan Mid Cap, the trust now pays four equal quarterly dividends, with a total that is equivalent to 4% of NAV as of July 31 each year, the end of the trust’s financial year. However, it is important to note that this has not changed the investment process – the team are happy to own stocks which do not pay a dividend if they feel they add value to the portfolio.

Performance has been incredibly strong over the past decade, with JUGI returning 187.1% (share price) compared with 114.5% for the IT UK Smaller Companies sector. It is also ahead of the sector from an NAV perspective (160.8% vs. 111.7%) *.

Why now for this portfolio?

- UK small-caps have remained at historically attractive valuations for a prolonged period

- Despite closing recently, JUGI remains at an attractive discount of 5.3%*

- Rising M&A has been a big boon for JUGI, with holdings being bought at premiums of 50-100%

- Dividend policy offers a great alternative to investors in this market

- Portfolio is well-diversified with exposure to medium and smaller-sized companies, as well as some AIM holdings

- Closed-ended structure allows JUGI to access some businesses worth £100-300m without liquidity concerns

Manager’s View

“We’ve been a broken record saying this so I can understand why people are saying why now. Firstly, it’s the longevity of these compelling valuations. Then you must consider the divergence in performance between UK and European small-caps. UK smaller companies are absolutely at the bottom range when compared with large-caps and their own history.”

Georgina is not the first UK small-cap manager to tell us just how attractive UK equities look outside of the FTSE 100 in recent years. She admits she has become a broken record, but when a manager with three-decades’ worth of experience tells you valuations are at their most attractive in her time on the trust, it is worth taking notice. There is a lot going on in the world, but should it be affecting these companies to this extent?

The reality is investors are starting to take notice. For the past couple of years, we have had an M&A smorgasbord of sorts. Despite the management duo’s focus on quality, they have also seen several bids on their holdings. It is also worth noting this is not just private equity, with large companies acquiring smaller businesses.

“We have been known to turn down bids, but some of our premiums have been 50-100% – that is very much tomorrow’s price today – which is what we want to get. We’ve had a couple where we were not sure if it was the right price, and we have discussed this with management who explained why this was the case,” says Georgina.

Examples of bids include cross-border FX company Alpha Group, which was taken over at a 55% premium, and Manchester-based engineering group, Renold, which was acquired by Morgenthaler Private Equity in late 2025.

Georgina says, despite getting a 100% premium on the share price, the team felt Renold was still cheap and an indictment of the current market. She says the CEO has done a great job of rescuing the business, but ultimately the share price had not moved. She says management persuaded them this was the best move for the business to grow. There were plenty of occasions where bids came in and Georgina would speak to the management of these businesses and say they should not have a discussion with the bidding firm unless there was a 100% premium – citing the dislocation in the share price.

The success of this M&A has been twofold: boosting the NAV on the trust and providing capital for new opportunities at a time when the sweetshop has been open for business.

A role reversal on buybacks

Share buybacks have surged in the UK because many companies are perceived as undervalued compared with global peers, prompting management to use surplus cash to boost share prices and earnings per share. Historically, this has been something Georgina was adamantly against, preferring companies to either return it as dividends or maintain a strong balance sheet. She says: “Liquidity is king for UK smaller companies, and I was wary that eating your own liquidity would put off putative investors.”

But things have changed, and valuations have reached such lows that she believes nothing could be more accretive for these companies than simply buying back their own shares.

The trust’s benchmark is the Numis Smaller Companies plus AIM (excluding Investment Companies) Index, which is roughly 60% mid-caps (JUGI currently holds 69%), meaning the portfolio has a strong exposure across mid, small and AIM companies. The closed-ended structure allows them to look at companies further down the market-cap spectrum (£100m to £300m), given they do not have the liquidity pressures of an open-ended vehicle.

Examples of holdings further down the market-cap scale include Nurcos (£260m), which is a supplier of high-quality bathroom and kitchen products, including tiles, adhesives, showers and taps. The company operates through a portfolio of well-known brands such as Triton Showers, Vado and Johnson Tiles, serving both residential and commercial markets.

Another is Science Group (£250m), a science-led consultancy and product development organization that provides technical, engineering and regulatory services to clients in the medical, defence, industrial, and food & beverage sector. Georgina says the firm continued to beat market expectations and has an incredibly strong balance sheet.

The VQM Model (Value, Quality, Momentum) for JUGI indicates the strength of the process, outperforming its index on all three metrics (see chart below).

Portfolio positioning

Recent additions and portfolio construction

There have been several additions to the portfolio in 2025. Examples include Boku, a global mobile payments company providing carrier billing and mobile identity solutions that enable consumers to make purchases and verify their identities using their mobile phones. Boku’s technology is integrated with major merchants, app stores and digital service providers. Georgina says the company was recording strong earnings momentum and remains an attractive growth prospect.

Another is construction company Galliford Try, which Georgina says is reaping the benefits from a turnaround programme with strong earnings and a growing order book.

Other names added include the likes of Curry’s and cyber security firm Intercede.

Contributors to performance in the past 12 months have been diverse: the top performer was Lion Finance (previously Bank of Georgia) which has recorded strong loan growth and revenues, as well as a high return on equity. The team believe that, despite the stellar performance, the holding remains good value.

Applied Nutrition and Renold both benefitted from bids in 2025, while defence stock Serco was third on the list.

JUGI also invested in Hochschild Mining, a business they felt was very undervalued by the market. The firm reported a significant increase in revenue and earnings in the first half of 2025, with revenue up about 33 % year-on-year and adjusted EBITDA up 27 %, which lifted confidence in its financial momentum. This was prior to the strong rally in gold and silver in the second half of the year.

In terms of detractors, Georgina says she was disappointed in positions in pharma and biotech trial specialist Hvivo, as well as cosmetic provider Warpaint London.

However, names like Ashtead Technology, Cerillion, Premier Foods and Trainline are businesses Georgina believes are struggling on sentiment and circumstance, with the underlying case remaining strong.

She says: “Premier Foods has never put a foot wrong – it never misses its numbers and has released a strong trading statement. Trainline remains an incredible tech company on 10x – a tech company should simply not be on that figure.”

Performance

Performance has been incredibly strong over the past decade, with JUGI returning 187.1% (share price) compared with 114.5% for the IT UK Smaller Companies sector. It is also ahead of the sector from a NAV perspective (160.8% vs. 111.7%)*.

Stock selection will be the main driver of performance, although the managers will highlight compelling value with this segment of the market, given the lowly valuations and volatility we have seen in recent years.

What else do investors need to know

The managers have a £55m one-year revolving credit facility, which can rise to £90m. JUGI will typically hold gearing between 8-10%, with the figure closer to 10% in recent years due the number of opportunities available to investors.

The discount on the trust has come down recently (currently 5.3%), having traded at an average discount of almost 10% for the past five years*. However, given the strong long-term performance of the trust, there is evidence to suggest this is still an attractive entry point from this perspective.

JPMorgan UK Small Cap Growth & Income’s charging structure looks to pass on the economies of scale to investors as they are achieved through a tiered management fee. The first £200m of net assets attracts a fee of 0.65%, with assets above this charged at 0.55%. Ongoing charges come in at 0.78% (company fees and expenses).

Outlook

This trust has produced extremely strong long-term performance across numerous time periods. A merger with the JPMorgan Mid Cap fund in 2024 has introduced several benefits, including better liquidity and pricing, while the trust also offers an enhanced dividend strategy, helping it to stand out from its peers.

We believe the managers’ bottom-up stock selection process of building a relatively concentrated portfolio of high-quality businesses further down the market-cap scale should continue to deliver strong performance, particularly at a time when small and mid-cap valuations remain at attractive levels.

JPMorgan UK Small Cap Growth and Income

Equity

*Source: AIC, as at 9 February 2026

This article is provided for information only. The views of the author and any people quoted are their own and do not constitute financial advice. The content is not intended to be a personal recommendation to buy or sell any fund or trust, or to adopt a particular investment strategy. However, the knowledge that professional analysts have analysed a fund or trust in depth before assigning them a rating can be a valuable additional filter for anyone looking to make their own decisions.

Past performance is not a reliable guide to future returns. Market and exchange-rate movements may cause the value of investments to go down as well as up. Yields will fluctuate and so income from investments is variable and not guaranteed. You may not get back the amount originally invested. Tax treatment depends of your individual circumstances and may be subject to change in the future. If you are unsure about the suitability of any investment you should seek professional advice.

Whilst FundCalibre provides product information, guidance and fund research we cannot know which of these products or funds, if any, are suitable for your particular circumstances and must leave that judgement to you. Before you make any investment decision, make sure you’re comfortable and fully understand the risks. Further information can be found on Elite Rated funds by simply clicking on the name highlighted in the article.

Related insights

Autumn 2025: the funds gaining and losing their Elite Ratings