Why tariffs are a red herring for the real emerging markets story

By Chris Salih on 23 July 2025 in Equities, Asia/Emerging Markets, Investment Trusts

A guide to JPMorgan Emerging Markets Investment Trust

Last year marked Austin Forey’s 30th anniversary as manager of the JPMorgan Emerging Markets Investment Trust (JMG). To mark the event, he highlighted a number of lessons that helped forge his approach to investing in the market. These included the evolution of the market; the idea economic growth does not mean superior returns; and the importance of valuations and cycles*.

However, there were two specific points which currently stand out. The first is that you must navigate for the future as markets continue to evolve. This is something we’ve seen with emerging markets (EMs) outperforming global markets year-to-date, the ongoing uncertainty around tariffs, value continuing to dominate growth and the changing fortunes of India and China.

The second is the need to take a long-term view, something which he says is criticised. Overlooking the long-term in the region is actually quite commonplace. For example, there is an average of 13 sell-side analysts making 1-year growth forecasts per stock in the region; by contrast there is typically just one doing this over 5-years**.

JMG tries to cut through the news by focusing on the growth of companies, rather than specific countries. Forey targets high-quality businesses that can outperform over a prolonged period of time and, as a result, the average company is held in the portfolio for 10 years, with a number of the larger positions held for an even greater period of time.

Forey is joined on JMG by fellow portfolio manager John Citron. Long-term performance has been strong, with a total return (share price) of 128.8%*** in the past decade (NAV has risen 119.7%)****, beating the MSCI Emerging Markets Index (95.6%)***.

Investment Process

The managers essentially want to answer two questions: Is this a business they want to own? And, if yes, what price are they willing to pay for it?

JMG has a very clear quality bias. The answer to the first question focuses on understanding the basic economics, duration, and governance of any company covered. The team conducts a strategic risk profile of every firm in its investment universe; companies which qualify are then analysed for their five-year expected returns (favouring companies driven primarily by earnings growth and dividends as they are within a company’s control) and the team then decides whether the shares are at a price it is willing to pay.

The managers are ably supported by a research team of almost 100 investment professionals from the Emerging Markets and Asia Pacific team. The team members speak more than 20 languages between them and conduct more than 3,000 interviews with company management each year.

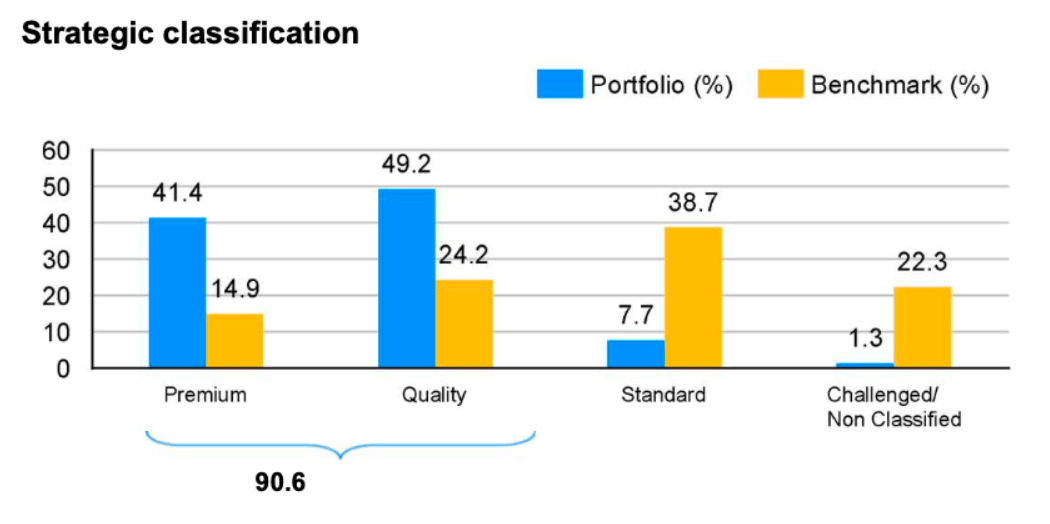

Companies are placed into four strategic categorisations: premium, quality, standard or challenged. The majority of JMG (over 90%) currently sits in the premium and quality buckets – and there are currently no challenged stocks. Given the lower-risk nature of premium and quality stocks, the managers are more tolerant of a lower expected return, because there is greater confidence in that return coming through. By contrast, a standard company must have a higher expected return, as there is more uncertainty around the numbers (ultimately there will be less patience).

The final portfolio holds between 50-80 stocks, with a turnover of around 10% — although this can be markedly lower.

Why now for this portfolio

- Excellent long-term track record of outperformance. Focus on higher returns on equity, stronger balance sheets and lower levels of debt has also helped JMG remain resilient in challenging periods.

- 12-month forward price-to-earnings premium on the portfolio (16x vs. 12.2x for the benchmark) is about as narrow as it has ever been**.

- Dollar weakness is a positive for emerging markets – specifically corporate earnings

- Long-term focus is under-represented in markets – meaning the team are happy to wait for performance.

- Market leading research team support JMG.

- OCF of 0.79% is the lowest in the IT Emerging Markets sector****.

Manager’s View

“I think tariffs are a red herring; the most important event in the last few months has been the US dollar. It has come down significantly (year-to-date) and for the first time in decades it fell in a risk-off environment.”

Tariff talk has dominated the headlines for the whole of this year. However, the research team at JPM has already taken steps to counteract this uncertainty. The analysts have now put into place tariff assumptions into all of their normalised numbers for all countries (with the exception of China which is clearly higher).

Claire Peck, investment specialist on JMG, says the market is not as exposed as people might think – citing lead manager Austin Forey’s view that the US consumer is likely to be the worst affected by the increases in cost and inflation. By contrast, many emerging markets revenue exposures are primarily towards their own domestic economies.

Peck says: “Indonesia, China, Philippines, Saudi Arabia, Turkey and India – anything between 75-90% of their revenue exposure of the MSCI EM Index is domestic, so that gives some insulation against US tariffs. The potential impact varies across regions. The most exposed are Korea and Taiwan – which are cyclical markets meaning they are more globally exposed. The other place which has been impacted positively is Latin America.”

She adds that China has also been preparing for a scenario of this ilk for some time – with the US representing only 3% of its exports.

The result is there have been very few tariff-driven changes. Peck believes tariffs are actually a red herring and that the performance of the US dollar (which has fallen 10% year-to-date^) is the real talking point for EMs.

As many will be aware, the dollar smile has been a heavily-used framework for FX investors for a number of years. When global growth is strong – the middle of the smile – the dollar tends to underperform other currencies, while in times of US outperformance or during a global recession, the US dollar is your friend. JPMorgan believes the smile is becoming more of a smirk, as it may no longer be a safe haven during times of distress.

Traditional dollar smile

Peck says: “The significance here is the US dollar got very expensive in a 15-year bull market. That is a really difficult environment for emerging market equities to perform in. If the US dollar goes into a multi-year consolidation, that is super positive for the rest of the world.”

What does this mean for emerging markets specifically? It means funding costs can go down, which stimulates growth and corporate earnings (which are translated into US dollars year-on-year) which all start to strengthen.

“It has removed the handcuffs on central banks in emerging markets to start to bring down rates. Brazil, Mexico, Indonesia, South Africa and others can start cutting rates which can stimulate both credit and domestic growth,” says Peck.

As mentioned, over 90% of JMG’s companies sit in the Premium or Quality bracket. That has been consistent in the portfolio over time, with India holding the highest number of premium names, while China has no premium companies at all.

Standard companies currently account for around 7.5% of the portfolio and are normally held for a valuation-led reason. A good example of this would be Korean stock Kia Motors, which Peck says looks attractive relative to other companies given the market it sits in and the current point of the cycle. Peck highlights “Korea’s corporate value-up programme” which has seen the government try to improve shareholder returns (in a similar vein to what is already happening in Japan). By contrast, it is only gathering pace under Korea’s new president.

Another standard holding would be Chinese giant Alibaba. Peck says the changing environment – alongside competition in the technology sector – means that while it may have previously sat in the quality bucket, it needed to move to the standard category.

The team have been adding selectively to high-quality holdings in recent times (see portfolio attribution and recent changes).

India and China – two behemoths with different prospects

China and India are the twin behemoths of emerging market investment. Together they make up almost half of the MSCI Emerging Market index. Their fortunes also have an impact on emerging markets more broadly – commodity demand from China will impact Brazil, for example, while Indian growth will impact South East Asia.

JMG has a structural underweight to China (18.1% vs. 25.9% for the benchmark)^^ which has been a bit of a lag on performance in the past 12 months, with stocks like shopping platform Meituan not part of the portfolio (however this has become more of a tailwind recently). Peck says, while there remain some very impressive businesses in China – which they are willing to invest in – the political risk remains an ever-present factor, and the economy is facing significant challenges as a result of over-investment and high levels of debt.

Read more: High risk, high reward: the case for (and against) China

India sits on the other end of the outlook, with Peck citing it as the last true emerging market in terms of both demographics and a runway for growth. She says the mid-cycle pause we have seen has helped valuations, although they are still relatively expensive.

She says: “India is uniquely positioned in a global context. It has waves of structural reforms, deregulation, financialisation and investment infrastructure by the government. The hope is private companies start to invest in infrastructure and that provides you with the next leg of the opportunity. Doing this with companies that are some of the best at turning that economic growth into earnings growth.”

An example of a long-term holding in this space is private bank HDFC, which sits in the premium bucket. Peck says the company did not participate as much in the rally in Indian equities, but remains convinced the investment case will deliver. Another recent addition is Praj Industries, an engineering company that is geared to the infrastructure story playing out.

Portfolio activity

Attribution and recent changes**

When looking at stock attribution year-to-date you can see a common theme on the detractors side in the shape of IT services, with names like Infosys, Globant, EPAM Systems and Tata Consultancy Services among the top 10. Peck says their forward-looking statements sounded relatively cautious and that the underperformance of these companies is reflecting the uncertainty around the US economy and whether companies will be spending the same way on outsourcing should the economic outlook slow. The role of AI in the future of these companies is also likely to have played a part.

Among the strongest attributors is Mercado Libre, the Latin American e-commerce and digital platform, which Peck says is not only the dominant player in its region – but has scope to venture into other areas.

Another is BBVA, which is a Spanish multinational financial services company, which earns a chunk of its profits in emerging markets like Mexico and Turkey. Rounding off the top three attributors year-to-date is Chinese gaming company NetEase, which has benefitted from more optimism towards (and money coming into) this specific market.

Limited changes reflect confidence in the portfolio

Portfolio turnover has been relatively low thus far in 2025. Names added include the likes of IT services company Coforge, which fits under the quality bracket. With a market-cap of $7.5bn it sits in the mid-cap sector, with the team seeing a lot of upside from here.

Another is SK Hynix, a North Asian tech (Korea) tech company, which Peck says is the leader in high band width memory, an area of growing demand due to AI. They have also added PB Fintech, a financial technology company that operates online platforms for insurance and lending products in both India and internationally.

Sales included Inner Mongolia Yili, a dairy company in China, as well as Ping An Insurance.

Performance

“You’ve now got a portfolio where the premium above the benchmark, in terms of the PE multiple, is about as narrow as it has ever been. Dividend yields (a quality cashflow measure) is just below the benchmark. But we have not had to compromise on the quality DNA of the portfolio.”

As mentioned, long-term performance has been strong, with both the share price (128.8%) and the NAV (119.7%) beating the MSCI Emerging Markets Index (95.6%)***.

Recent performance has been slightly challenging, with Peck pointing to volatility and the value-driven market of the past few years – led by many of the low-quality stocks JMG avoids. However, the makeup of the portfolio, as evidenced by the chart below, demonstrates the resilience of JMG, which has only slightly underperformed the benchmark over the past three years (14.3% vs. 20.6% for the MSCI Emerging Markets Index)^^^.

| Portfolio** | Benchmark** | |

| 12-Month Forward Price to Earnings (x) | 16.0 | 12.2 |

| Price to book (x) | 3.4 | 1.8 |

| Dividend yield (%) | 2.4 | 2.7 |

| Return on equity (%) | 18.4 | 12.6 |

| Net debt to equity (%) | -9.4 | 21.7 |

There were some individual stock challenges in both India and China. Some names held by JMG in India were private sector financials, which did not participate in the strong rally to the same degree as a number of growth companies.

China has naturally been a challenge given the issues facing the market in recent years. Peck says some companies which were classified as quality or even premium did not deliver, citing Foshan Haitian Flavouring & Food Co. Ltd, a condiments company, as an example. Consumer and internet companies also had over optimistic earnings growth assumptions – which Peck says reflected natural behaviour biases around the outlook when things were going well.

“Ultimately, there has been a structural change in the world’s second largest economy, with earnings growth not reflecting the new situation in the country. Consumer confidence collapsed post-Covid, with the real estate bubble also being burst.”

The team have been going through the earnings growth numbers on China, with stress-testing and revisions being made. They have also made enhancements on top of their process. While the initial four steps (strategic classification, checklist (98 questions on a stock), materiality framework and the five-year expected returns forecast) remain in place, they have also introduced an industry framework – a macroeconomic overlay to make sure the individual numbers for companies are realistic – to help the team sanity check individual company numbers in a wider context.

“We’ve also introduced pre-determined game plans – these are signposts for what analysts are tracking to ensure the investment case remains on track. Even when we take long-term views, having those checkpoints for thesis drift is very important,” Peck adds.

What else do investors need to know

- Having been double digits for much of the past 18 months, the discount has narrowed to 8% recently, which is markedly below the average discount of 9.2% over the past five years. However, it remains wider than the average for the IT Global Emerging Market sector (-4.15%).

- The board will consider share buybacks if they believe they are in shareholders’ best interests.

- JMG can use up to 20% gearing but currently has no facility in place, with the managers keen to leave the stocks to do their work over a prolonged period of time.

- Although the primary focus is on total return over generating a particular level of income, JMG has managed to maintain or grow its dividend for the majority of the past decade. Earnings rose to 2.12p per share in the last financial year.

Outlook

Peck says the portfolio is in an excellent position to tap into a number of structural trends impacting the region. Roughly a third is in technology, where North Asian tech companies, in countries like Korea and Taiwan, are underpinning the AI story by producing the component parts. Another is exposure to financials, which plays into the domestic growth story as emerging market countries start to bring down rates to spur domestic growth. The third theme is exposure to the consumer and communications. Crucially, all three look in a better position today because the US dollar has come down.

Backed by one of the largest emerging market research teams, manager Austin Forey has delivered excellent returns on this trust for more than three decades, emphatically demonstrating his long-term approach to stock picking has been successful, whilst also being able to evolve this portfolio to meet changing trends. The focus on quality underpins that success, giving investors protection in challenging periods.

The chart above demonstrates just how much of an outlier the portfolio is to the wider MSCI Emerging Market index. This, coupled with the focus on the long term, means that now could well be a very attractive entry point.

*Source: JPMorgan Asset Management

**Source: trust presentation, June 2025

***Source: FE Analytics, total returns in pounds sterling, 21 July 2015 to 21 July 2025

***Source: Association of Investment Companies, 21 July 2025

^Source: MarketWatch, 21 July 2025

^^Source: fund factsheet, 30 June 2025

^^^Source: FE Analytics, total returns in pounds sterling, 21 July 2022 to 21 July 2025

This article is provided for information only. The views of the author and any people quoted are their own and do not constitute financial advice. The content is not intended to be a personal recommendation to buy or sell any fund or trust, or to adopt a particular investment strategy. However, the knowledge that professional analysts have analysed a fund or trust in depth before assigning them a rating can be a valuable additional filter for anyone looking to make their own decisions.

Past performance is not a reliable guide to future returns. Market and exchange-rate movements may cause the value of investments to go down as well as up. Yields will fluctuate and so income from investments is variable and not guaranteed. You may not get back the amount originally invested. Tax treatment depends of your individual circumstances and may be subject to change in the future. If you are unsure about the suitability of any investment you should seek professional advice.

Whilst FundCalibre provides product information, guidance and fund research we cannot know which of these products or funds, if any, are suitable for your particular circumstances and must leave that judgement to you. Before you make any investment decision, make sure you’re comfortable and fully understand the risks. Further information can be found on Elite Rated funds by simply clicking on the name highlighted in the article.

Related insights

Are the clouds clearing for emerging markets?

Four reasons to back emerging markets from here

Is it time to bag an investment trust bargain?